The $850B global small business insurance market is broken. SMBs face a paradox: they need insurance to survive, but the complexity of choosing the right coverage—health, liability, property, cyber, workers' comp—causes analysis paralysis. Traditional brokers serve enterprise clients profitably, leaving SMBs to navigate 200+ page policy documents alone.

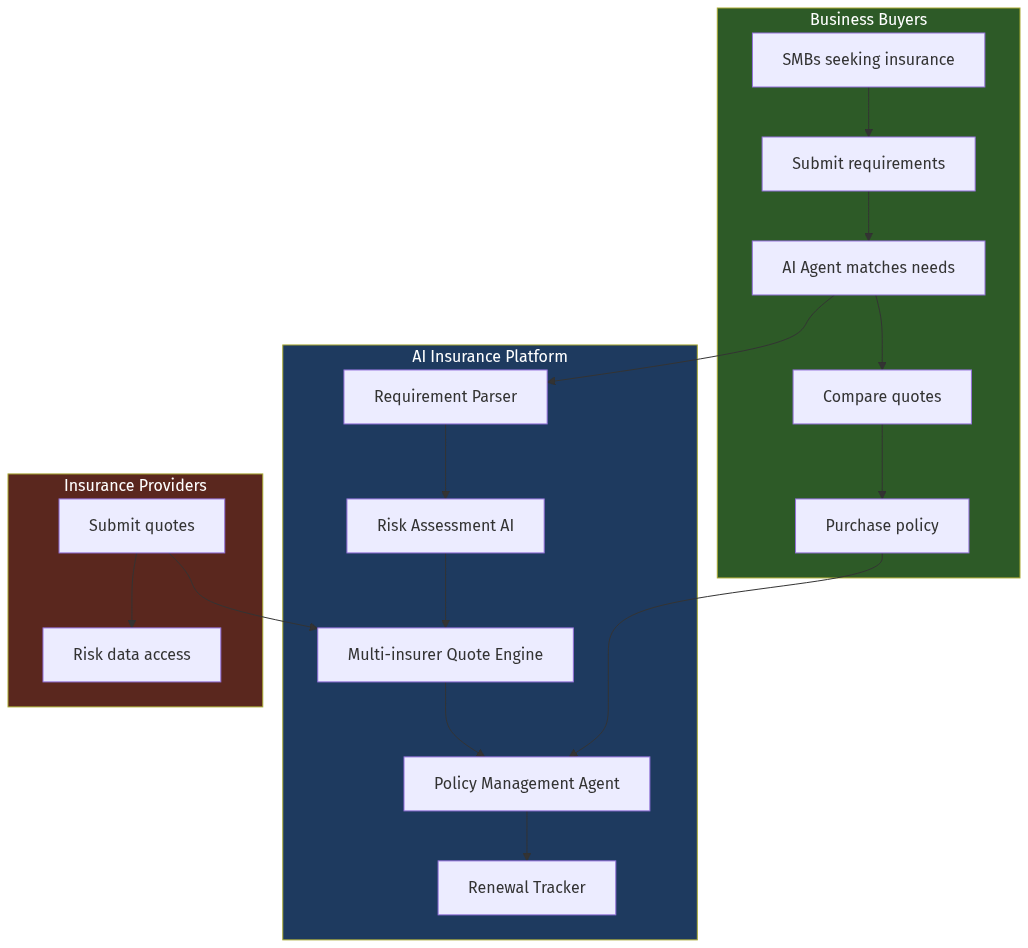

This creates a massive opportunity for AI-powered insurance marketplaces that act as intelligent intermediaries. Instead of human brokers who handle 50 accounts, AI agents can handle 50,000, providing instant quotes, personalized recommendations, automated claims, and proactive renewal management.

Global SMB insurance market: $850B (2025), projected $1.2T by 2030 (8% CAGR) India SMB insurance gap: $45B in unmet coverage needs Average broker commission: 15-25% of premium (can be reduced to 5-8% with AI)The inflection point: India's 63 million SMBs are going digital. UPI payments crossed $3T in 2025. GST compliance is near-universal. The infrastructure for AI-driven insurance is ready—the market just needs the interface.