Applying Incentive Mapping: The legacy FAP market operates on a perverse incentive—providers profit from finding errors, not preventing them. The more complex and error-prone the invoicing ecosystem, the more valuable audit services become. This creates little incentive to actually fix the root cause.

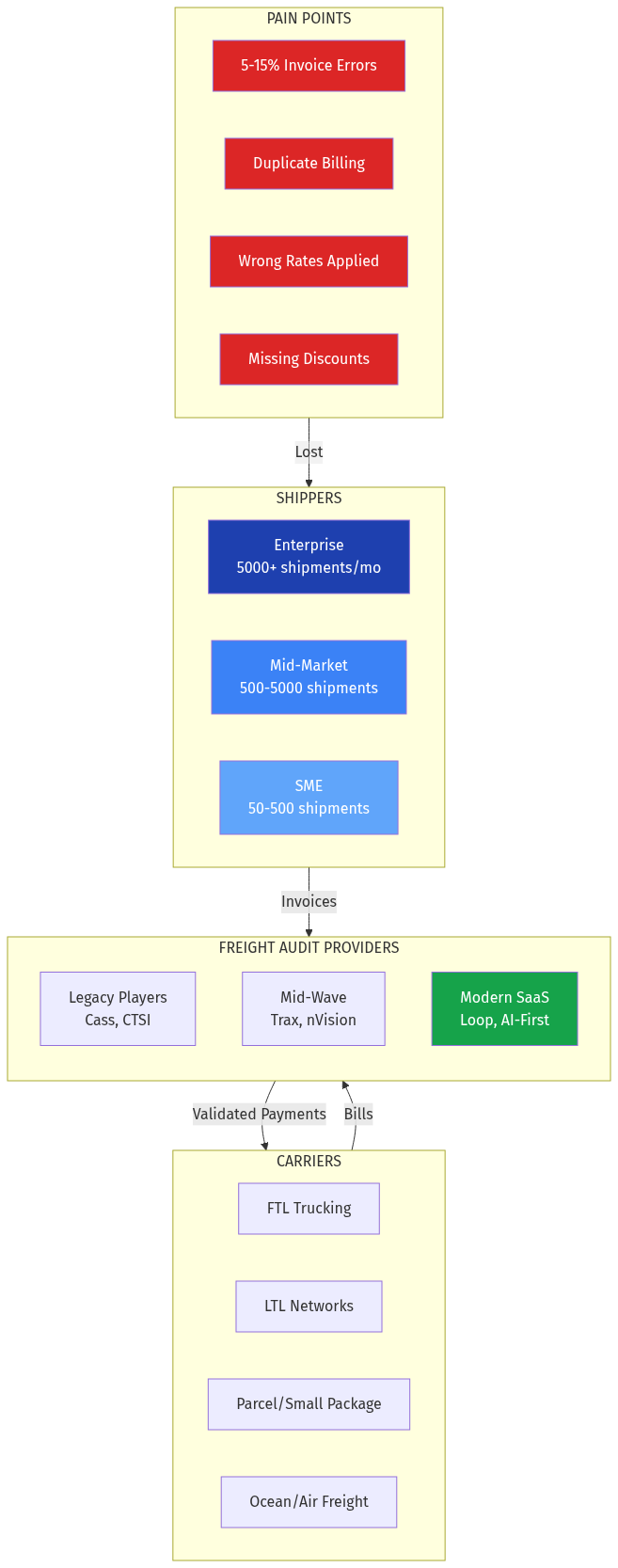

| Cass Information Systems | 1906 | Full-service FAP, utility bills | Legacy tech, enterprise-only pricing, slow implementation |

| CTSI-Global | 1955 | Transportation analytics + FAP | Consulting-heavy model, not self-serve |

| Trax Technologies | 1993 | Global FAP + business intelligence | Complex implementation, 6-12 month onboarding |

| nVision Global | 1992 | Multi-mode FAP + TMS | Traditional service model, limited AI |

| Intelligent Audit | 1996 | Parcel-focused audit | Narrow mode coverage, not AI-native |

| Loop | 2021 | AI-powered SaaS FAP | North America only, limited modes |

| Blume Global | 1994 | TMS + FAP integrated | Heavy TMS lock-in required |

The Legacy Model Problem

Applying Distant Domain Import (from SaaS disruption): The FAP industry mirrors where accounting software was before Xero/QuickBooks disrupted it—dominated by consultants, complex implementations, and per-transaction pricing that punishes growth.

Legacy providers typically:

- Charge per invoice processed (incentivizes complexity)

- Require 6-18 month implementations

- Need dedicated client teams for exception handling

- Operate on 1990s-era rule engines, not ML

- Bundle FAP with unnecessary consulting services

Loop (2021) represents the modern approach: SaaS pricing, fast implementation, and claims 99% touchless approval. But they're North America-only and limited to parcel/LTL/TL. The global, multi-modal opportunity remains open.