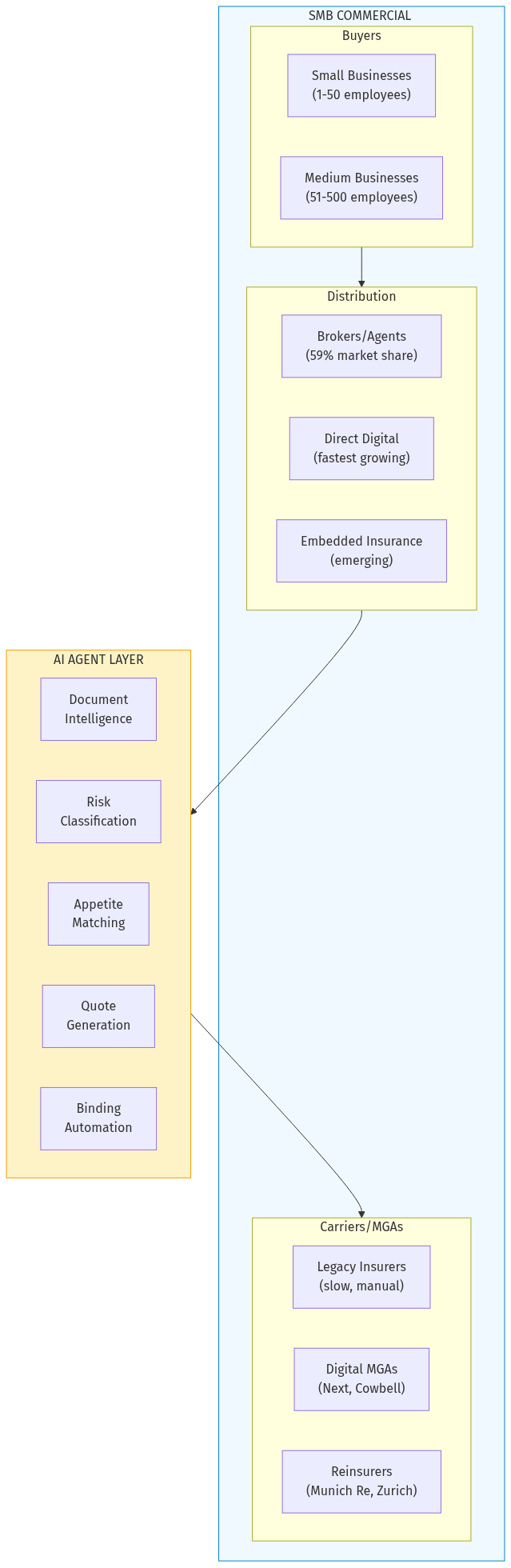

The global commercial insurance market stands at $922 billion in 2025, projected to reach $1.35 trillion by 2030 at a 10% CAGR. Yet the SMB segment—small businesses seeking general liability, property, cyber, and workers' compensation coverage—remains dramatically underserved due to the economics of manual underwriting.

The core problem: It costs carriers the same to underwrite a $5,000 premium small business policy as a $500,000 enterprise account. Traditional underwriters spend 30-40% of their time on administrative tasks, leaving only ~30% for actual risk assessment. The result? SMBs face 8-12 day quote-to-bind cycles, complex applications, and coverage gaps. The AI opportunity: Autonomous AI agents can handle document ingestion, risk classification, appetite matching, and quote generation in minutes instead of days. Early movers like Next Insurance ($4B valuation), Cowbell ($208M raised), and NeuralMetrics are proving the model, achieving 60-99% faster quotes and 3-5% loss ratio improvements.This represents a rare convergence: a trillion-dollar market, clear workflow automation potential, and proven AI capabilities—yet incumbent carriers are still wrestling with legacy systems. The window is open.