India's industrial water treatment chemicals market generated $1.05 billion in 2024 and is projected to reach $1.8 billion by 2033 — a 7.3% CAGR driven by Zero Liquid Discharge (ZLD) mandates, urbanization, and industrial expansion.

Yet the market structure is a paradox: sophisticated chemical engineering meets primitive procurement. Factories still order coagulants and biocides via WhatsApp messages to local distributors. Invoicing is manual. Compliance documentation is assembled retroactively from scattered logs. Payment cycles stretch 60-90 days.

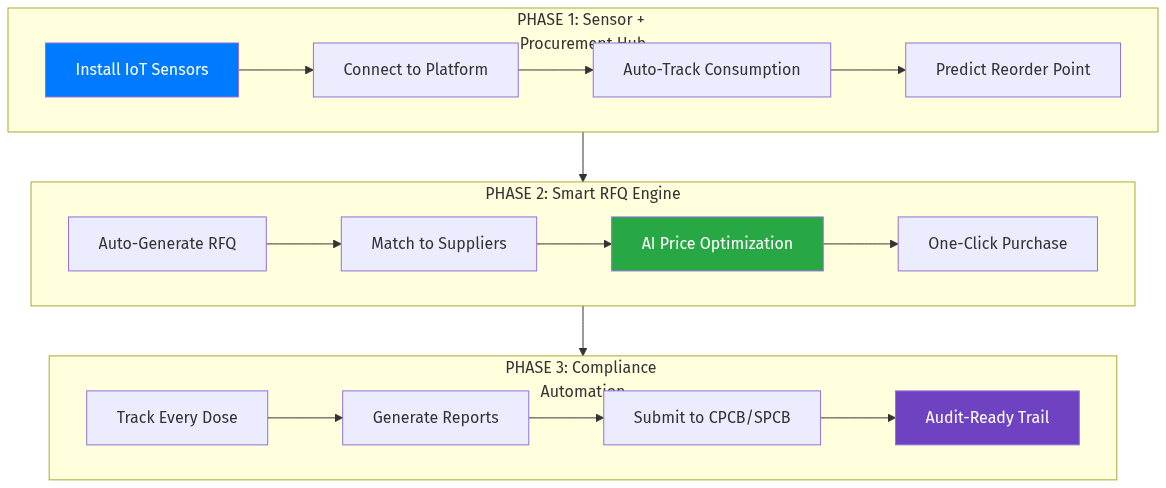

The opportunity is a full-stack AI procurement platform that connects IoT-enabled smart dosing systems to an intelligent supplier marketplace, generating automatic reorders, optimized pricing, and audit-ready compliance trails. Think "Stripe for water chemicals" — where every dose is tracked, every purchase is optimized, and every regulatory report is auto-generated.