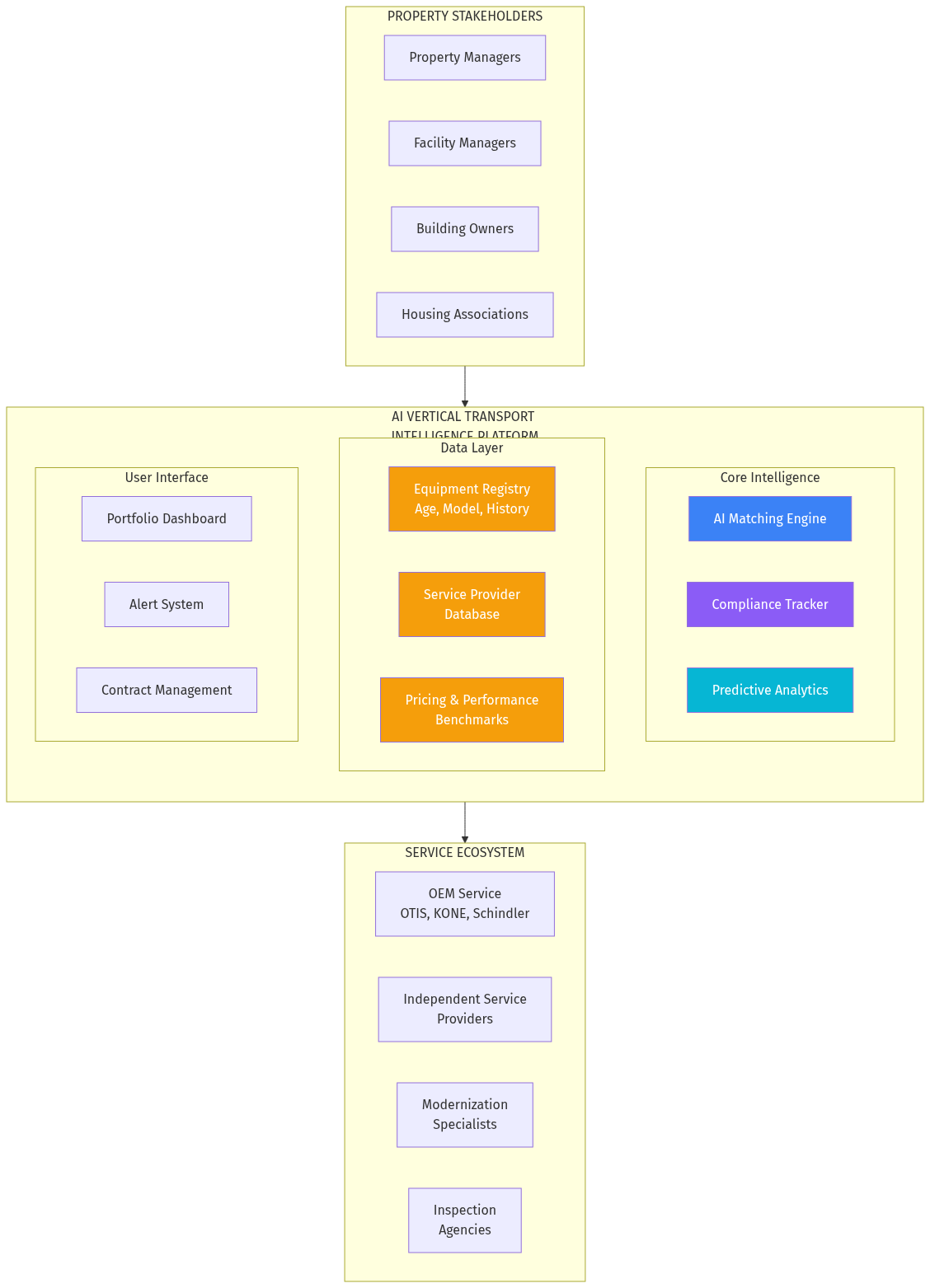

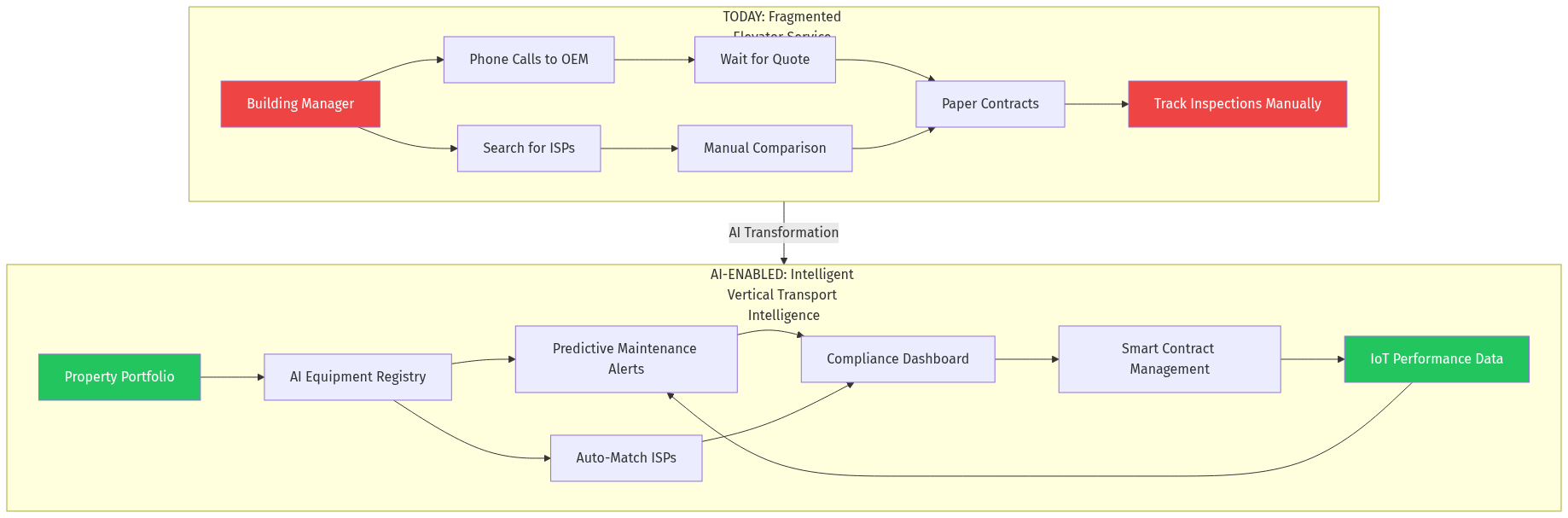

The global elevator and escalator market is projected to reach $113.8 billion by 2030, with maintenance and repair services comprising approximately 30-35% of industry revenue — a $35B+ addressable market growing at 4-5% annually. Despite this scale, vertical transport service procurement remains fragmented, opaque, and largely offline.

Property managers juggle multiple service providers, track compliance certificates manually, and have no visibility into whether they're paying market rates. Meanwhile, independent service providers (ISPs) struggle to compete against OEM-captured accounts despite often offering comparable quality at 20-40% lower cost.

An AI-enabled vertical transport service intelligence platform can transform this market by creating transparency, automating compliance, and enabling data-driven service provider matching — while building a proprietary database that becomes more valuable with every transaction.