Strategic Alignment

B2B Marketplace DNA: Trade finance is the ultimate B2B transaction layer—without financing, trade doesn't happen

AI-Native Opportunity: Document AI, credit scoring, and matching engines are core AI capabilities aligned with AIM's technology stack

India-First, Global-Second: India's $45B export credit market is underserved; success here proves model for global expansion

Network Effects Match AIM Philosophy: More exporters → better buyer data → more lender participation → more exporters

Potential AIM Integrations

- niyukti.in (Recruitment): Finance staffing costs for export-oriented manufacturers

- instabox.in (Logistics): Embedded financing for freight costs

- thefoundry.in (Industrial): Working capital for machinery procurement against export orders

- masale.in (Ingredients): Commodity trade finance for spice exporters

Domain Opportunity: tradefinance.in

A premium, exact-match domain that signals authority in the space. Current holder should be approached for acquisition.

## Pre-Mortem: Why This Might Fail

FALSIFICATION EXERCISE

Assume five well-funded startups tried this and failed. Why?

Credit losses exceeded projections

-

Risk: AI models overfit to training data, fail on new buyer populations

-

Mitigation: Conservative advance rates (70-80%), mandatory credit insurance for new buyers, continuous model retraining

Lender concentration killed economics

-

Risk: One or two lenders dominate, extract all margin

-

Mitigation: Enforce lender diversity quotas, vertical integration option (warehouse facility)

Regulatory shutdown

-

Risk: RBI classifies as unregulated lender, requires NBFC license

-

Mitigation: Pure marketplace model, no balance sheet lending, clear regulatory legal opinions

Document fraud evolved faster than AI

-

Risk: Fraudsters adapt techniques to bypass detection

-

Mitigation: Human review for high-value/high-risk, consortium approach to fraud intelligence sharing

Banks copied and won

-

Risk: HDFC/ICICI launch similar product with distribution advantage

-

Mitigation: Multi-bank positioning, speed-to-market, proprietary data moats banks can't replicate

STEELMANNING: Best Argument Against This Opportunity

"Trade finance exists in equilibrium. Banks profit from complexity, SMEs accept it because they have no alternative, and regulators don't prioritize reform. Any disruptor faces three incumbents simultaneously: banks who control lender relationships, large corporates who prefer anchor programs, and regulators who instinctively protect banking intermediation. The $2.5T gap isn't a market failure—it's a feature that maintains banking profitability."

Counter-argument: This equilibrium held because alternatives didn't exist. AI changes the cost structure so dramatically that a new equilibrium becomes possible—one where alternative lenders (NBFCs, funds, ECAs) can serve the SME segment profitably through an intelligent intermediary.

## Verdict

Opportunity Score: 8.5/10

| Market Size | 9/10 | $2.5T gap, $9T overall market |

| Pain Intensity | 9/10 | Working capital is existential for exporters |

| AI Leverage | 9/10 | Document AI, credit scoring, matching engines |

| Competitive Moat | 7/10 | Data moat strong but requires scale to build |

| Execution Risk | 6/10 | Regulatory, credit risk, lender concentration |

| AIM Fit | 9/10 | Perfect alignment with B2B marketplace thesis |

Final Assessment

This is a high-conviction opportunity for the following reasons:

The problem is acute and quantified: $2.5 trillion gap is not theoretical—it's rejected applications from real SMEs

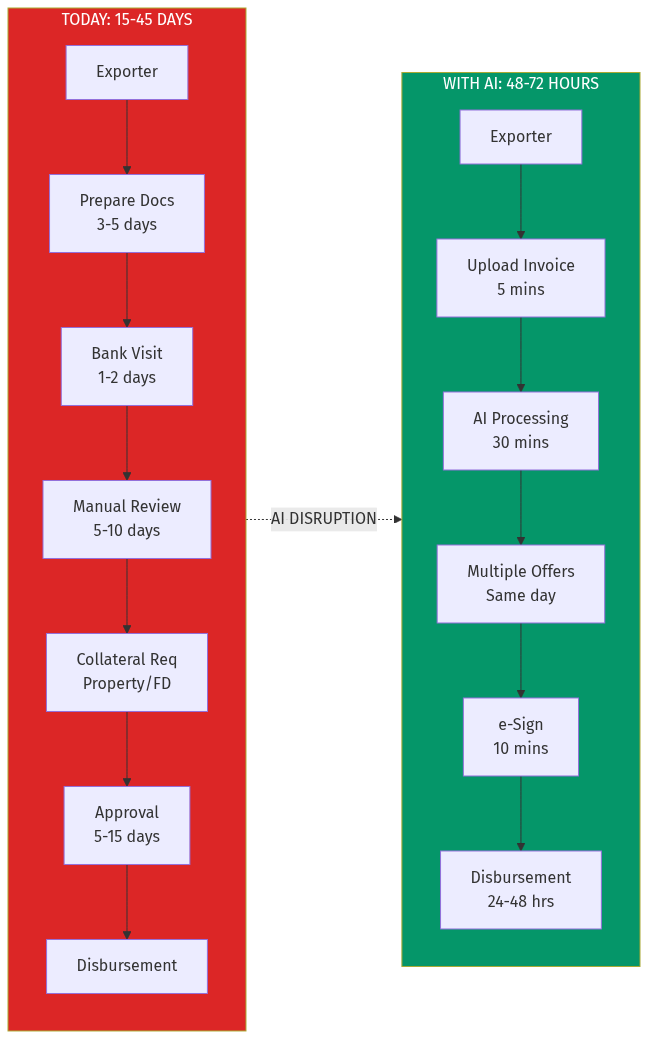

AI fundamentally changes unit economics: What costs $500-2000 to underwrite manually can be done for $5-20 with AI

The timing is right: Document AI, alternative data, and regulatory frameworks have all matured simultaneously

Network effects create defensibility: Buyer payment data and lender matching intelligence compound over time

Recommended next step: Validate with 10 SME exporter interviews and 3 NBFC conversations to confirm willingness to transact on the platform.

## Sources