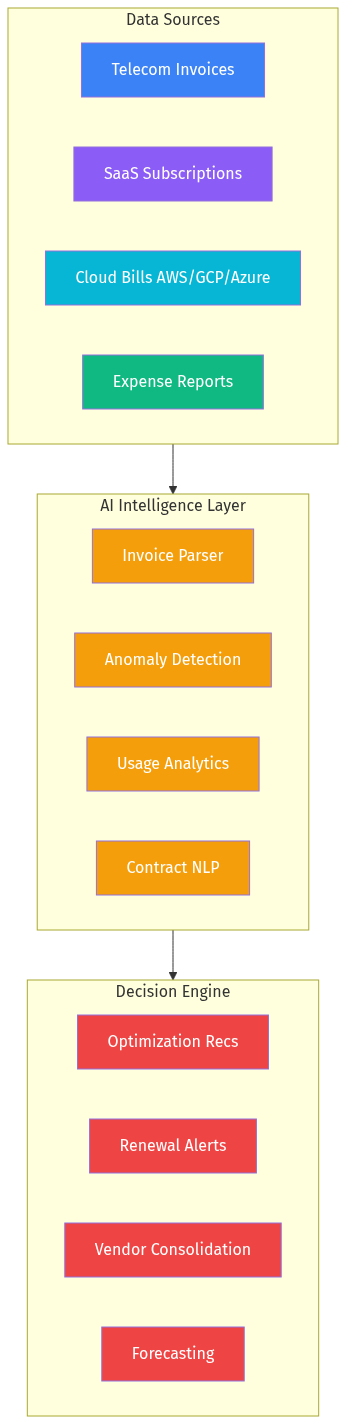

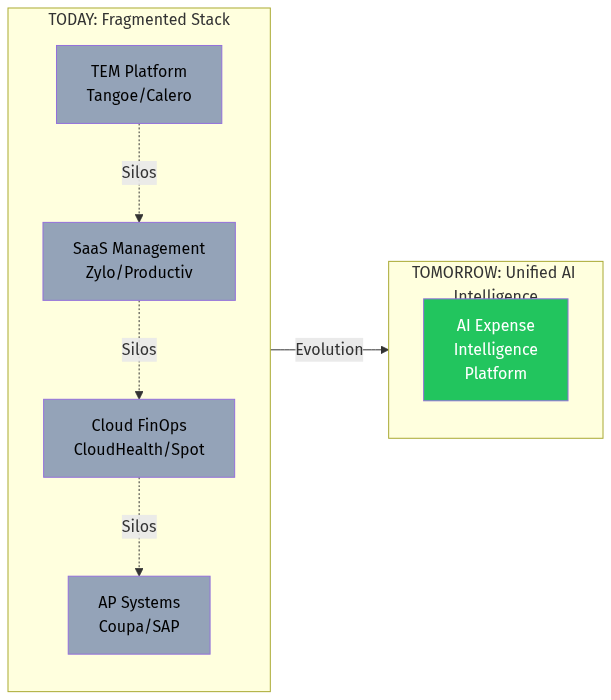

Technology expense management is a $47 billion problem hiding in plain sight. Enterprises manage telecom, SaaS subscriptions, and cloud costs through 3-4 separate platforms that don't talk to each other. Finance teams manually reconcile thousands of invoices. IT has no visibility into shadow SaaS. Procurement can't negotiate effectively without usage data.

The opportunity: Build an AI-native platform that ingests ALL technology expenses (telecom, SaaS, cloud, hardware), automatically parses contracts, detects anomalies, and generates actionable optimization recommendations. Unlike legacy TEM (Telecom Expense Management) platforms built for the 2010s, this would be the first truly unified technology expense intelligence platform.

Why now: The convergence of three trends—LLMs capable of parsing complex contracts, API-first SaaS vendors exposing usage data, and CFO pressure on software ROI—creates a window for a new category leader.