Strategic Alignment

AIM's thesis: Structure beats scale. Build intelligence layers for fragmented B2B markets.

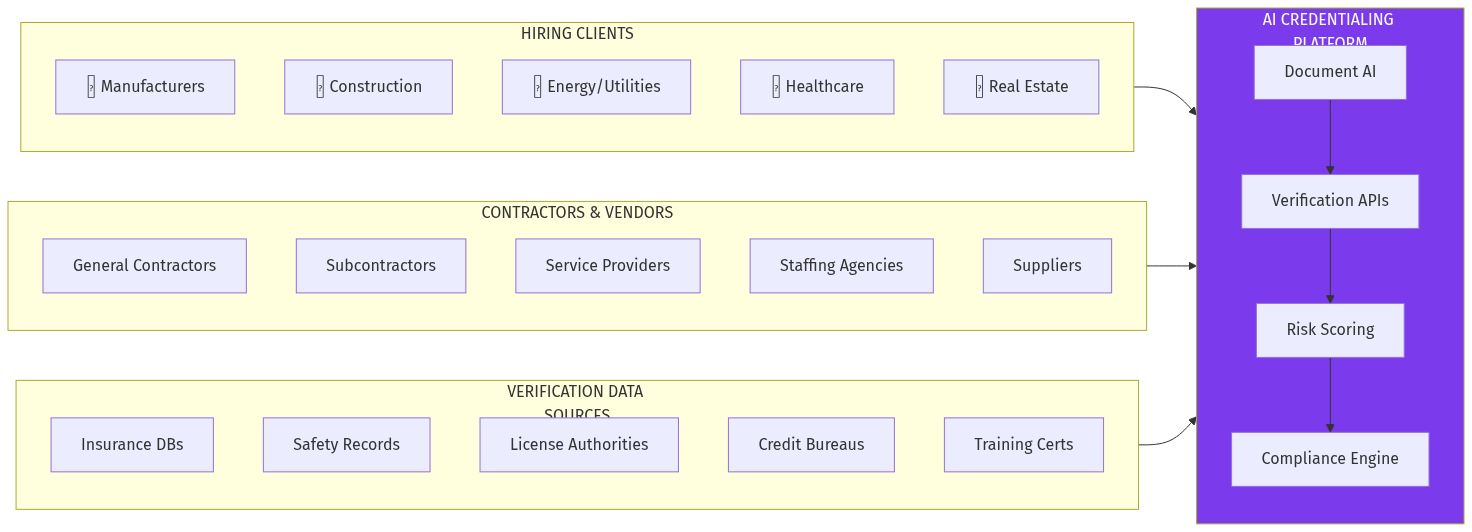

Contractor credentialing is:

- Highly fragmented (thousands of clients, millions of contractors)

- Data-rich (every credential is structured information)

- Transaction-heavy (continuous verification cycles)

- Trust-critical (compliance = liability management)

Integration Opportunities

- thefoundry.in - Industrial procurement often requires contractor credentials

- niyukti.in - Staffing/recruitment with credential verification layer

- instabox.in - Logistics contractors require driver/vehicle credentialing

Domain Assets

- credentials.in, credentialing.in (potential acquisitions)

- verify.in, verified.in

- contractor.in, vendors.in

## Pre-Mortem: Why This Could Fail

Failure Mode 1: Incumbent Retaliation

ISNetworld and Avetta have 70,000+ clients combined. They could:

- Slash prices to lock in customers

- Acquire AI capabilities through M&A

- Bundle credentialing into larger procurement platforms

Mitigation: Move faster than they can adapt. Their legacy architecture and business model are structural constraints.

Failure Mode 2: API Access Barriers

Real-time insurance and license verification requires carrier/authority cooperation.

Mitigation: Start with public data sources, build volume, negotiate API access with demonstrated value.

Failure Mode 3: Contractor Adoption Friction

Contractors already pay for multiple platforms. Another one may face resistance.

Mitigation: Free tier for contractors, demonstrate value through faster onboarding and new client discovery.

Failure Mode 4: Regulatory Complexity

Credentialing requirements vary by state, industry, and client.

Mitigation: Start with common requirements (insurance, OSHA), expand to specialized credentials with industry-specific modules.

## Steelmanning: Why Incumbents Might Win

Best case for ISNetworld/Avetta:

Network effects are real - 70K clients and 12M contractors is a massive moat

Switching costs are high - Clients have built workflows around existing platforms

Compliance inertia - "Nobody got fired for buying ISN"

AI can be bolted on - Incumbents could acquire or build AI capabilities

Counter-argument:

Network effects matter less when the product experience is 10x worse. Switching costs decrease when the new solution offers data portability. Compliance teams want better tools—they're not loyal to platforms that cause pain.

The credentialing industry is ripe for disruption precisely because incumbents are complacent.

## Verdict

Opportunity Score: 8.5/10

Strengths

- Massive market ($7.2B+) with clear pain points

- AI creates 10x efficiency improvement over manual review

- Per-contractor pricing model is vulnerable to platform disruption

- High switching costs work both ways—once clients adopt AI-first, they won't go back

- Strong data moat potential from document processing volume

Weaknesses

- Incumbent network effects are real barriers

- API access for real-time verification requires partnerships

- Multi-industry complexity increases development scope

Recommendation

Build the insurance verification wedge first. COI tracking is the highest-pain, fastest-ROI feature. Use it to land customers, then expand to full credentialing.

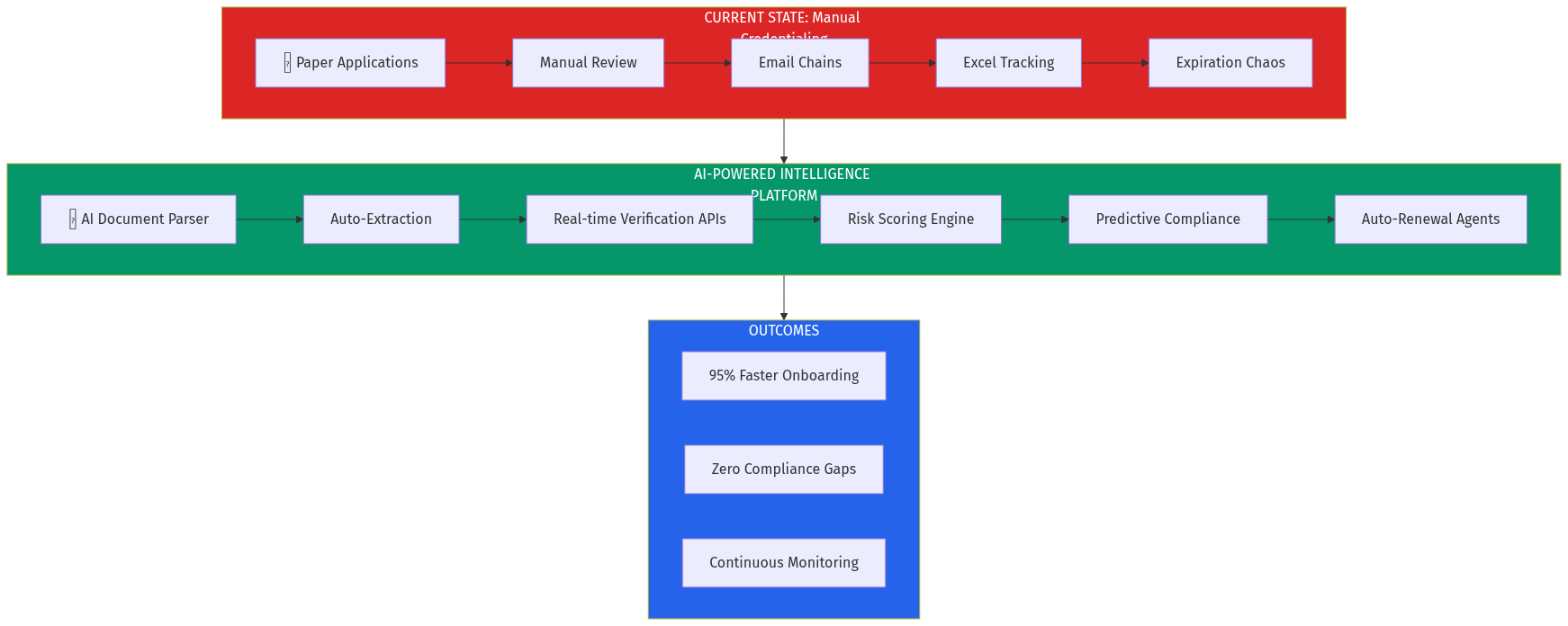

The credentialing market is a $12B opportunity trapped in manual workflows. AI agents don't just improve the process—they fundamentally change the economics. Incumbents charging $1,000/contractor/year will struggle to compete with platforms delivering better outcomes at $50/contractor.

The question isn't whether this market gets disrupted. It's who does it first.

## Sources