Alignment with AIM.in Vision

B2B Workflow Transformation

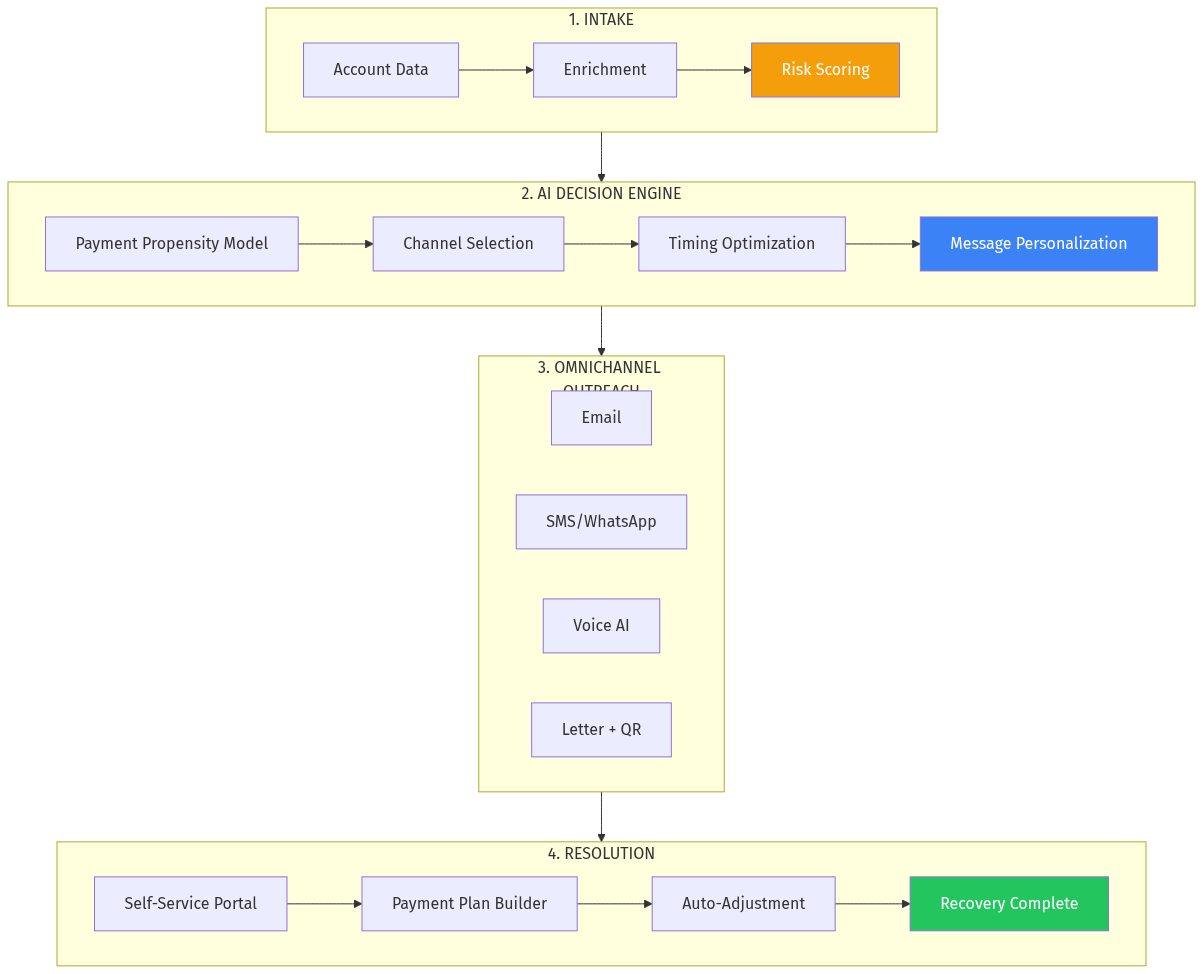

- Collections is a fragmented, offline-heavy workflow

- Perfect fit for AI-first marketplace thinking

India-First Opportunity

- WhatsApp + UPI + Account Aggregator = unique Indian stack

- Digital lending boom creating massive collections need

- Regulatory tailwinds (RBI pushing for dignified practices)

Ecosystem Effects

- Creditors using AIM for procurement could use same platform for AR

- Financial services vertical (networth.in) natural integration

- Cross-sell to existing AIM relationships

Domain Portfolio Leverage

- Potential domains: collect.in, recover.in, dues.in, ar.in

Second-Order Thinking: What Happens If This Succeeds?

- Direct: $10M+ ARR business within 3 years

- Indirect: Data moat enables credit scoring product

- Second-order: Creditors trust AIM with financial operations → expand to AP automation

- Third-order: Become the "Stripe of B2B money movement" for India

## Verdict

Opportunity Score: 8.5/10

Strengths

- Massive, proven market ($13.6B US, growing in India)

- Clear pain point with misaligned incumbents

- AI advantages are demonstrable and defensible

- Regulatory tailwinds (digital channels now permitted)

- WhatsApp + UPI creates India-specific moat

Risks

- Long sales cycles with enterprise creditors

- Compliance complexity requires domain expertise

- Channel risk (WhatsApp policy changes)

- Reputation management (collections = negative associations)

Recommendation

Build this. Start with SaaS dunning (low friction, clear ROI) and expand to digital lenders in India. The WhatsApp + Account Aggregator stack is a genuine differentiation that US competitors can't easily replicate. The market is large enough to support multiple winners, and AIM's B2B positioning provides natural creditor relationships.

The mental model that unlocks this: Collections is a UX problem disguised as a finance problem. Whoever solves for debtor dignity at scale wins.

## Sources