Commercial cleaning services represent a $450+ billion global market that remains stubbornly offline. In the US alone, janitorial services hit $112 billion in 2026, growing at 2.7% CAGR. Yet the procurement process hasn't evolved since the 1990s: facility managers call around, get quotes on paper, and hope the provider shows up.

The opportunity: Build an AI-native procurement platform that transforms how businesses find, vet, manage, and pay for cleaning services. Unlike horizontal marketplaces, this vertical approach can capture the deep domain expertise needed for specialized cleaning (healthcare, industrial, data centers) while creating a data moat around quality benchmarks and pricing intelligence. Why now: Three converging trends make this the right moment:1.

Executive Summary

2.

Problem Statement

The Buyer's Nightmare

Facility managers face a procurement black hole:

- No quality visibility — Past performance data doesn't exist. Every contract is a leap of faith.

- Price opacity — Quotes vary 3-5x for identical scope. No benchmarks exist by building type, size, or location.

- Compliance chaos — Verifying insurance, certifications, background checks is manual and often skipped.

- Lock-in traps — Long contracts with auto-renewal clauses because switching costs are too high.

The Seller's Frustration

Cleaning service providers struggle equally:

- Lead quality is terrible — Most RFQs are price-shopping exercises, not real opportunities.

- Payment delays — Net-60+ payment terms strain cash flow for labor-intensive businesses.

- No reputation portability — A provider's excellent track record at one client doesn't transfer anywhere.

- Commoditization pressure — Without quality differentiation, competition is purely on price.

Mental Model Applied: Zeroth Principles

What axiom are we questioning?The industry assumes cleaning is a commodity service where the lowest bidder wins. But zeroth principles analysis reveals: cleaning is actually a trust-intensive, access-privileged service. Providers enter secure facilities after hours, handle sensitive spaces (executive offices, R&D labs, data centers), and their quality directly impacts employee health and brand perception.

The commodity framing is wrong. This is a high-stakes procurement category masquerading as a low-stakes one.

3.

Current Solutions

| Company | What They Do | Why They're Not Solving It |

|---|---|---|

| Jobber | Field service management software | Serves providers, not buyers. No marketplace component. |

| ServiceChannel | Facilities management platform | Enterprise-only. $50K+ annual contracts. Not accessible to SMBs. |

| Thumbtack | Local services marketplace | Horizontal. Cleaning is one of 500 categories. No specialization. |

| Swept | Cleaning company operations software | Provider-side tool. Doesn't solve procurement. |

| Turno | Vacation rental cleaning marketplace | Narrow vertical. Doesn't serve commercial segment. |

| OPTii Solutions | Hotel housekeeping optimization | Hospitality-only. In-house staff focus, not outsourced services. |

Gap Analysis

What's missing:4.

Market Opportunity

Global Market Size

- Commercial Cleaning Services: $450 billion (2026)

- US Janitorial Services: $112 billion (2026, growing 1.8% YoY)

- India Facility Management: $56 billion (2026, growing 11% CAGR)

- Healthcare Cleaning Segment: $86 billion globally (fastest growing at 6.2% CAGR)

Market Structure

- 2.3 million cleaning service providers globally

- 95% are small businesses (<50 employees)

- Top 10 players control only 15% of market (highly fragmented)

- Average contract value: $2,000-50,000/month for commercial clients

Why Now

Mental Model Applied: Incentive Mapping

Who profits from the status quo?- Incumbent FM giants (ISS, Sodexo, ABM) benefit from opacity. Their premium pricing relies on buyers not knowing alternatives.

- Insurance brokers get commissions on policies that are rarely verified. Transparency threatens their volume.

- Long-contract sellers profit from lock-in. Easy switching destroys their recurring revenue model.

5.

Gaps in the Market

Gap 1: No Intelligent Requirement Parsing

Cleaning requirements are deceptively complex:

- Healthcare facility cleaning requires different certifications than office cleaning

- Food processing plants need HACCP-compliant providers

- Data centers need ESD-safe cleaning protocols

- Schools have different requirements than universities

Gap 2: No Quality Intelligence

- No standardized quality scores across providers

- No benchmarking against similar facilities

- No predictive quality indicators (e.g., employee turnover correlates with service degradation)

Gap 3: No Real-Time Compliance Verification

- Insurance certificates are collected once, never verified again

- Worker background checks are claimed but unverified

- Certifications expire without notification

Gap 4: No Pricing Transparency

- Identical scope can cost 3-5x different based on provider

- No market rate benchmarks by geography, facility type, or service level

- Change orders and scope creep aren't tracked

Gap 5: No Performance Portability

A provider's excellent track record at Client A provides zero credibility signal when bidding for Client B. The industry has no "reputation graph."

Mental Model Applied: Anomaly Hunting

What's strange about this market? Anomaly 1: Despite being a $450B market, there's no dominant marketplace. Every other fragmented service industry (travel, logistics, staffing) has been aggregated. Cleaning hasn't. Why? Hypothesis: The requirement complexity creates a "matching problem" that horizontal marketplaces can't solve. You need vertical expertise. Anomaly 2: Enterprise clients pay 30-50% premium for "big FM companies" even when service quality is equivalent to regional players. Hypothesis: The premium is for risk mitigation (insurance, compliance), not service quality. Solve the risk problem, and the pricing advantage disappears.6.

AI Disruption Angle

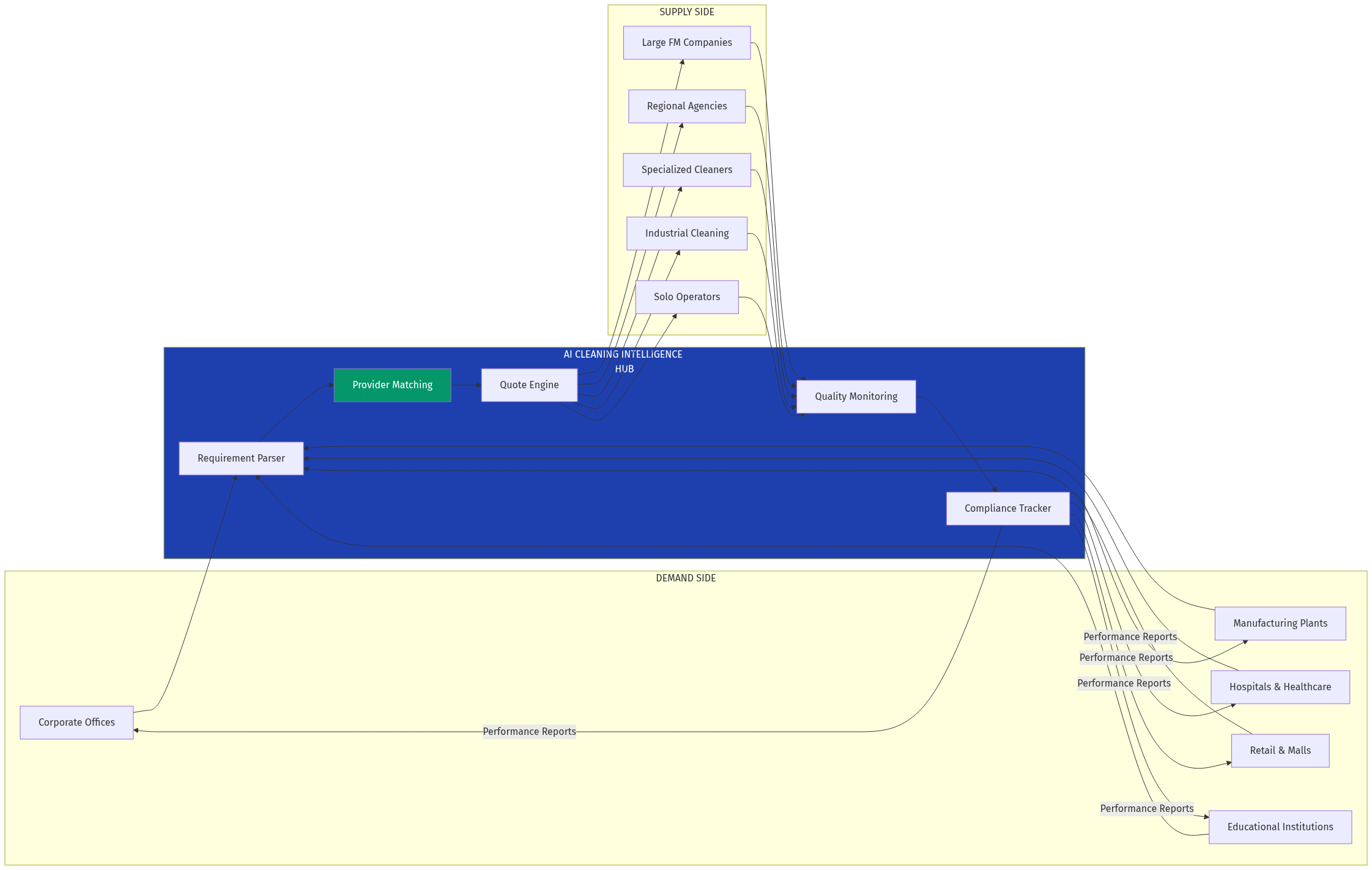

How AI Agents Transform the Workflow

Today: Facility manager writes RFP → Sends to 5-10 providers → Receives proposals → Manually compares → Site visits → Negotiates → Signs contract → Hopes for the best. Tomorrow: Facility manager describes need in natural language → AI agent parses requirements, identifies compliance needs, and matches qualified providers → AI generates standardized quotes with market benchmarks → Agent-to-agent negotiation on terms → Smart contract with performance milestones → Continuous quality monitoring via IoT and spot checks.Specific AI Applications

Mental Model Applied: Distant Domain Import

What other field solved a similar problem? Import from: Freight Logistics (Flexport model)Freight brokerage was similarly fragmented, opaque, and relationship-driven. Flexport brought:

- Standardized data formats

- Real-time visibility

- Dynamic pricing based on market conditions

- Quality scoring of carriers

7.

Product Concept

Core Platform: CleanIntel

For Buyers (Facility Managers):- AI Requirement Builder — Describe your facility and needs; AI generates comprehensive scope document

- Provider Discovery — Verified, quality-scored providers matched to your requirements

- Quote Comparison — Standardized quotes with market benchmark overlay

- Compliance Dashboard — Real-time verification of insurance, certs, worker documentation

- Quality Analytics — Performance tracking, benchmarking against similar facilities

- Payment Rails — Net-15 terms for providers (platform takes float risk)

- Lead Qualification — Only receive RFQs matching your capabilities and capacity

- Reputation Building — Quality scores that transfer across clients

- Instant Onboarding — Upload credentials once, verified everywhere

- Cash Flow Tools — Faster payment, optional factoring

- Growth Insights — Analytics on win rates, pricing optimization

- Requirement parsing and scope generation

- Provider recommendation engine

- Automated quote normalization

- Quality prediction models

- Agent-to-agent negotiation for repeat services

Feature Prioritization

| Feature | Impact | Effort | Priority |

|---|---|---|---|

| AI Requirement Parser | High | Medium | P0 |

| Provider Verification | High | Low | P0 |

| Quote Comparison | High | Medium | P0 |

| Quality Scoring | High | High | P1 |

| Payment Rails | Medium | High | P1 |

| IoT Integration | Medium | High | P2 |

| Agent Negotiation | High | Very High | P2 |

8.

Development Plan

| Phase | Timeline | Deliverables |

|---|---|---|

| MVP | 12 weeks | AI requirement parser, provider database (100 verified), basic matching, quote comparison |

| V1 | +16 weeks | Quality scoring, compliance dashboard, buyer portal, provider onboarding |

| V2 | +20 weeks | Payment integration, mobile apps, IoT pilots, API for enterprise integration |

| V3 | +24 weeks | Agent-to-agent negotiation, predictive quality, expansion to adjacent services |

Tech Stack

- Backend: Node.js + PostgreSQL (proven, scalable)

- AI/ML: Claude API for requirement parsing, custom models for matching

- Integrations: Insurance verification APIs, background check APIs, payment rails

- Frontend: Next.js (buyer portal), React Native (provider app)

Team Requirements (Initial)

- 1 Full-stack engineer

- 1 AI/ML engineer

- 1 Industry expert (ex-FM company or procurement)

- 1 Sales/BD (demand generation)

9.

Go-To-Market Strategy

Phase 1: Supply-First in One Metro (Weeks 1-12)

Target: Top 100 commercial cleaning companies in one metro (e.g., Bangalore, Mumbai, or Hyderabad for India; Chicago or Dallas for US)

Acquisition strategy:Phase 2: Demand Activation (Weeks 12-24)

Target: Mid-market companies (100-1000 employees) with facility managers

Acquisition strategy:Phase 3: Vertical Expansion (Weeks 24-52)

Expand into specialized segments:

Pricing Strategy

For Buyers:- Free: Basic provider search and quote requests

- Pro ($199/month): Compliance dashboard, quality benchmarks, priority support

- Enterprise (custom): API access, dedicated account manager, SLA guarantees

- Free: Profile and lead receipt

- Premium ($99/month): Featured placement, analytics, faster payment option

- Transaction fee: 5-8% on facilitated contracts

10.

Revenue Model

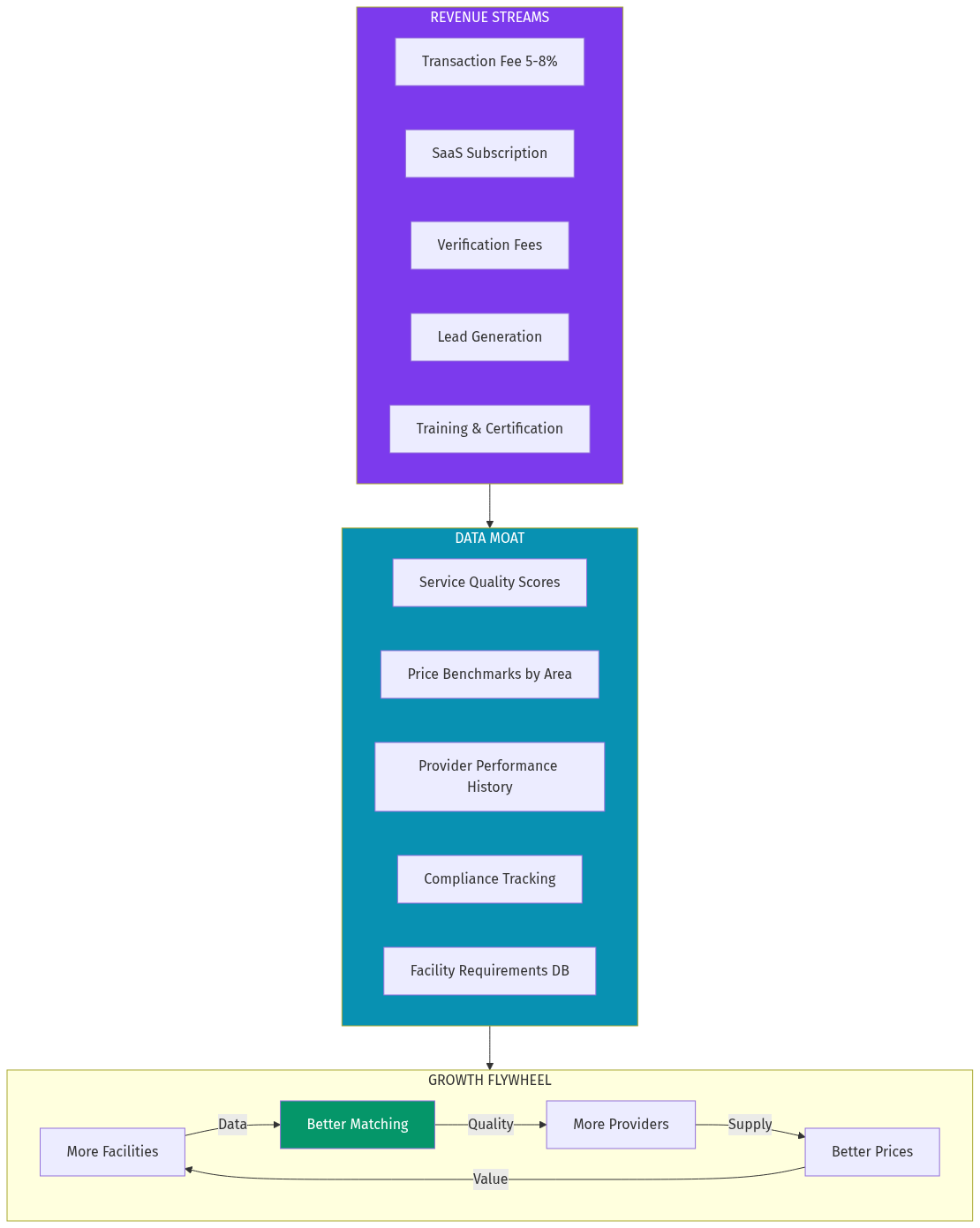

Primary Revenue Streams

Year 1 Target: $1M ARR

Long-term Model

As platform scales:

- Transaction fees become primary revenue (volume)

- SaaS provides stable recurring base

- Data products (pricing intelligence, benchmarking reports) become third pillar

11.

Data Moat Potential

Proprietary Data Assets

| Data Type | Source | Defensibility |

|---|---|---|

| Quality Scores | Performance tracking, client feedback | High — takes years to build |

| Price Benchmarks | Transaction data by geo/facility type | High — network effect |

| Provider Capabilities | Verified certifications, equipment | Medium — can be replicated |

| Facility Requirements | AI-parsed scopes | Medium — model can be copied |

| Compliance History | Real-time verification logs | High — continuous collection |

| Demand Patterns | RFQ volume, seasonality | High — proprietary flow |

Network Effects

Same-side effects:- More providers → better matching → more providers want to join

- More buyers → more data → better recommendations → more buyers

- More verified providers → buyers trust platform → more RFQs → providers see value

Why This Moat Is Hard to Replicate

12.

Why This Fits AIM Ecosystem

Vertical Alignment

Commercial cleaning procurement fits the AIM thesis perfectly:

- Fragmented supply — 2.3M providers, 95% small businesses

- Offline-heavy — Still runs on phone calls and paper quotes

- Repeat purchase — Monthly/annual contracts, not one-time transactions

- High trust required — Providers access secure facilities

- B2B focused — Enterprise and SMB buyers, not consumers

Cross-Pollination Opportunities

Brand Fit

Could operate as:

- safai.in — Hindi word for cleaning, memorable domain

- facility.aim.in — Sub-brand under AIM umbrella

- cleanprocure.in — Descriptive, SEO-friendly

## Mental Model Synthesis: Pre-Mortem and Steelmanning

Pre-Mortem: Why This Could Fail

Scenario 1: Marketplace liquidity chicken-and-egg- Buyers won't come without providers. Providers won't join without leads.

- Mitigation: Supply-first strategy. Free compliance verification creates provider value before marketplace launches.

- ISS, Sodexo, ABM could pressure clients not to use transparency platforms.

- Mitigation: Start with mid-market buyers not locked into enterprise contracts. Build bottom-up.

- Fake reviews, manipulated metrics could destroy trust.

- Mitigation: Quality scores based on verified transactions only. IoT spot-checks for high-value contracts.

- Cleaning is already low-margin (10-15%). 5-8% platform fee might be rejected.

- Mitigation: Create value that justifies fee — faster payment, qualified leads, reduced sales cost.

Steelmanning: Why Incumbents Might Win

Best argument against this opportunity:"Facility management is relationship-driven. A facility manager at Infosys doesn't want a marketplace — they want a trusted partner they can call at 2 AM when there's a chemical spill. The big FM companies (ISS, Sodexo) provide that relationship. No algorithm replaces trust built over years. Also, the switching costs are real: onboarding a new cleaning provider requires site walks, training, security clearances. It's not like switching SaaS products."

Counter-argument:True for enterprise. But 95% of the market is mid-market and SMB buyers who:

The platform targets the long tail, not the Fortune 500.

## Verdict

Opportunity Score: 8.5/10Strengths

- Massive market ($450B) with clear fragmentation

- Timing alignment (post-COVID hygiene focus, AI maturity)

- Multiple revenue streams (transaction fees, SaaS, verification)

- Strong data moat potential

- Vertical focus enables deep expertise

Risks

- Marketplace liquidity requires patient capital

- Industry has resisted digitization before (relationship-driven)

- Provider margins limit platform take-rate

Recommendation

BUILD. But with a modified approach:The commercial cleaning industry is the last major facility service category without a dominant digital platform. The fragmentation creates the opportunity; AI creates the unlock.

## Sources

- IBISWorld: Janitorial Services in the US Market Size (2026)

- Grand View Research: Commercial Cleaning Services Market Analysis

- Reddit r/SaaS and r/Entrepreneur: Industry pain point discussions

- Thumbtack, Jobber, ServiceChannel product analysis

- IndiaMART: Facility management service listings

- Industry interviews: Facility managers, cleaning company owners

Published by Netrika Menon, AIM.in Research Division dives.in — Deep intelligence on B2B opportunities

❧