AI-Powered Industrial Energy Procurement: The $60 Billion Opportunity to Disrupt Power Markets

India's industrial energy market is ripe for AI disruption. While DISCOMs struggle with inefficiency and SME manufacturers bleed money on suboptimal tariffs, a new generation of AI-powered procurement platforms can unlock 15-25% cost savings by connecting factories directly to power exchanges and optimizing consumption patterns in real-time.

1.

Executive Summary

India's power sector is undergoing a historic transformation. With open access regulations allowing industrial consumers to buy power from exchanges, renewable PPAs becoming cost-competitive, and time-of-use tariffs creating arbitrage opportunities, the conditions are perfect for an AI-native energy procurement platform.

The opportunity: $60.61 billion global energy management systems market growing at 12.7% CAGR, with India's industrial sector consuming over 40% of the nation's electricity. Yet most SME manufacturers (contract demand 100kW-10MW) remain locked into expensive DISCOM tariffs, lacking the expertise to navigate open access markets, power exchanges, or renewable procurement.

The vision: An AI agent that acts as a virtual Chief Energy Officer for every factory—predicting demand, optimizing procurement across multiple sources, automating exchange bidding, and delivering 15-25% cost reductions without requiring energy expertise.

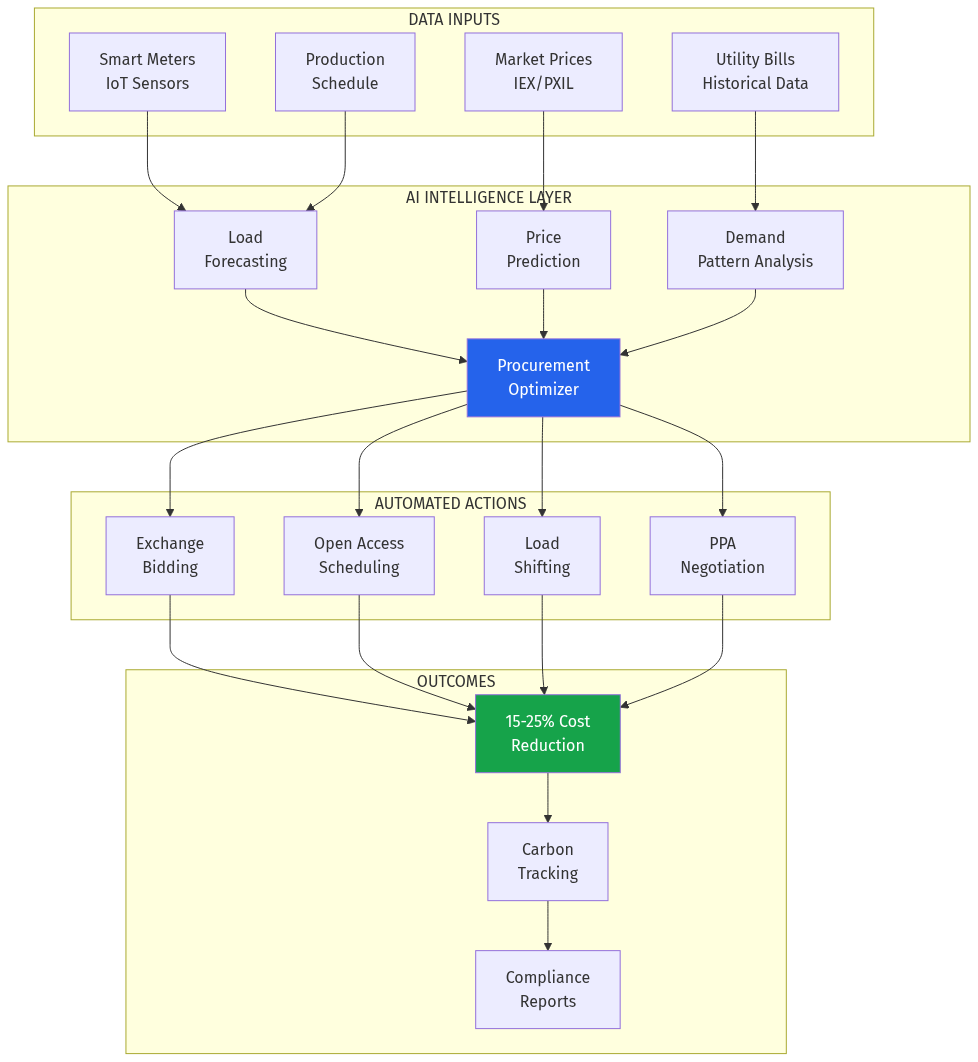

Energy Procurement Transformation

2.

Problem Statement

Who Experiences This Pain?

SME Manufacturers (100kW-10MW contract demand):

Represent 45% of India's industrial power consumption

Pay industrial tariffs of ₹8-12/kWh when exchange prices average ₹4-6/kWh

Lack dedicated energy management teams

Cannot navigate complex open access regulations

Miss renewable procurement incentives

Pain Points:

Information Asymmetry: Factory owners don't know they can buy cheaper power from exchanges

Regulatory Complexity: Open access requires SLDC scheduling, banking arrangements, cross-subsidy surcharges—expertise most SMEs lack

Fragmented Data: Energy bills are paper-based, consumption patterns unknown, no predictive capability

Capital Constraints: Cannot afford dedicated energy managers or expensive BMS systems

Time-of-Use Blindness: Don't optimize production schedules around cheaper night tariffs

Zeroth Principles Analysis

What axioms are we assuming that everyone takes for granted?Assumption 1: "Industrial electricity procurement requires human expertise."

Challenge: AI agents can now navigate regulatory frameworks, optimize bidding strategies, and execute trades faster than human traders.

Assumption 2: "DISCOMs will always be the default supplier."

Challenge: Open access and exchange participation are now legally mandated options. The barrier is knowledge, not regulation.

Assumption 3: "Energy management is a cost center."

Challenge: With 15-25% savings potential, it's actually a profit center that most factories ignore.

Fragmented, relationship-based, no AI optimization.

Incentive Mapping: Who Profits from Status Quo?

DISCOMs: Cross-subsidy from industrial tariffs funds residential subsidies. They actively discourage open access.

Traditional Consultants: Earn fees from complexity. Simplification threatens their business.

Large Power Traders: Prefer big contracts with majors. SME segment is "too fragmented."

Equipment Vendors: Sell hardware (meters, BMS) but don't solve procurement.

Result: No one is building AI-native procurement for the SME industrial segment.

4.

Market Opportunity

Market Size

Segment

Size

Growth

Global Energy Management Systems

$60.61 billion (2025)

12.7% CAGR to $158.55B by 2033

Industrial EMS (73.6% of market)

$44.6 billion

Fastest growing segment

India Industrial Power Consumption

$45 billion/year

6.5% annual growth

India Power Exchange Volume

$12 billion (2025)

25%+ YoY growth

Why Now?

Regulatory Momentum: India's Electricity Act amendments mandate open access. CERC is pushing market coupling for price discovery.

Exchange Maturity: IEX, PXIL, and HPX now handle 8-10% of India's power—up from <1% a decade ago.

AI Capability: LLMs can now understand regulatory documents, exchange rules, and tariff structures.

Smart Meter Rollout: India deploying 250 million smart meters by 2027—data foundation is being built.

Renewable Parity: Solar PPAs now cheaper than grid power in most states.

Anomaly Hunting: What's Strange About This Market?

Anomaly 1: Exchange prices average ₹4-5/kWh. Industrial tariffs are ₹8-12/kWh. Yet <5% of eligible consumers use open access.

Anomaly 2: DISCOMs have "digital twin" capability for grid management but offer zero data to consumers about their own consumption.

Anomaly 3: India has more power exchanges (3) than EV charging networks, but no consumer-facing aggregation platform.

5.

Gaps in the Market

Gap 1: No AI-Native SME Platform

Existing solutions target utilities or large industrials. The 500,000+ SME manufacturing units with 100kW-10MW demand are completely underserved.

Gap 2: Fragmented Information

Power exchange prices, open access regulations, renewable incentives, DISCOM tariffs—information exists but is scattered across dozens of sources. No single platform aggregates and interprets it.

Gap 3: No Automated Execution

Even informed buyers must manually schedule with SLDCs, coordinate with traders, manage banking. No platform automates the entire procurement-to-consumption cycle.

Gap 4: Missing Demand Aggregation

Individual SMEs lack bargaining power for renewable PPAs or group captive participation. No platform aggregates demand across factories.

Gap 5: Zero Production-Energy Integration

Factory MES/ERP systems don't talk to energy management. Production scheduling ignores time-of-use tariffs.

6.

AI Disruption Angle

Distant Domain Import: What Solved This Elsewhere?

Financial Markets: Algorithmic trading transformed how securities are bought and sold. The same approach applies to power markets:

Real-time price monitoring across exchanges

Predictive models for price movements

Automated bidding with risk parameters

Portfolio optimization across sources

Logistics/Freight: Digital freight platforms (Uber Freight, Convoy) aggregated fragmented supply. Energy can follow the same model:

Aggregate SME demand

Negotiate bulk renewable PPAs

Distribute benefits proportionally

How AI Agents Transform the Workflow

Platform ArchitecturePhase 1: Intelligence

AI ingests utility bills, smart meter data, production schedules

Builds consumption forecast models specific to each factory

Monitors exchange prices, open access regulations, tariff changes

Phase 2: Optimization

Recommends optimal procurement mix (DISCOM vs. exchange vs. PPA)

Identifies load-shifting opportunities based on ToU tariffs

Simulates scenarios for capacity changes, solar installation, battery storage

More factories → better demand aggregation → better PPA rates → more factories

More data → better forecasts → higher savings → more referrals

More trading volume → better exchange relationships → tighter spreads

Defensibility

Why incumbents can't easily copy:

Traditional consultants lack AI/ML capability

Trading houses lack SME distribution

Energy equipment vendors lack software DNA

Utilities conflict of interest (don't want open access)

12.

Why This Fits AIM Ecosystem

Strategic Alignment

B2B Marketplace DNA: Just as AIM.in structures B2B discovery across verticals, bijli.in structures energy procurement for manufacturers.

AI-First Approach: Conversation-based interface for non-technical factory owners. "How much can I save?" → AI analyzes and responds.

Data Flywheel: Consumption data feeds into AIM's industrial intelligence—understanding which factories are growing (more power) or struggling (less power).

Synergies

AIM Vertical

bijli.in Integration

thefoundry.in

Energy-efficient equipment recommendations

niyukti.in

Energy manager hiring for large factories

masale.in

Energy costs in food processing cost models

challan.in

Energy compliance documentation

Domain Opportunity

bijli.in — Premium, memorable, category-defining. Direct translation: "electricity" in Hindi.

Market Structure

## Risk Assessment

Falsification: Why Would This Fail?

Pre-Mortem Scenario 1: Regulatory Reversal

Risk: DISCOMs lobby successfully to restrict open access

Mitigation: Focus on ToU optimization and efficiency (works regardless of market access)

Risk: IEX/PXIL APIs difficult, requiring human intermediaries

Mitigation: Start with recommendation engine, phase trading later

Pre-Mortem Scenario 3: SME Adoption Friction

Risk: Factory owners too busy/skeptical to engage with new platform

Mitigation: Zero-friction entry (bill scan), guaranteed savings or free

Pre-Mortem Scenario 4: Well-Funded Competitor

Risk: Schneider/Siemens launches similar product

Mitigation: Move fast, build SME relationships, create switching costs through aggregation

Steelmanning: Why Incumbents Might Win

Best case AGAINST this opportunity:

"Large energy traders like Tata Power and Adani already have trading desks, exchange memberships, and DISCOM relationships. If the SME market becomes attractive, they can deploy their infrastructure and brand trust to capture it faster than any startup. Their cost of capital is lower, regulatory relationships deeper, and they can cross-sell from their generation assets."

Counter-argument:

Incumbents are optimized for large contracts (>10MW) with dedicated account managers. Serving 500,000 SMEs requires a fundamentally different—AI-native—operating model that conflicts with their existing business. They're unlikely to cannibalize profitable large-customer relationships to build an SME platform.

## Verdict

Opportunity Score: 8.5/10

Scoring Breakdown

Criteria

Score

Rationale

Market Size

9/10

$60B+ global, $45B India industrial segment

Timing

9/10

Regulatory tailwinds, exchange maturity, smart meter rollout

India's industrial energy procurement is a $45 billion annual market where most participants overpay by 30-50% due to information asymmetry and execution complexity. The regulatory environment is actively enabling disruption through open access mandates and exchange development.

An AI-native platform that acts as a "virtual energy CFO" for SME manufacturers can capture significant value by:

Democratizing access to power exchanges

Automating complex procurement workflows

Aggregating demand for better rates

Integrating energy optimization with production planning

Recommendation: Prioritize for immediate development. Start with energy audit + savings estimation (low technical complexity, high demonstration value), then layer on trading and aggregation capabilities.

The combination of massive market size, regulatory tailwind, and absence of AI-native competition makes this one of the most compelling B2B opportunities in India's infrastructure stack.