B2B trade credit is the invisible backbone of global commerce — $6 trillion outstanding at any moment. Yet collections remains stuck in the 1990s: spreadsheets, phone calls, threatening letters. The result? 10-15% of invoices paid late, 3-5% written off as bad debt, and countless business relationships destroyed in the pursuit of payment.

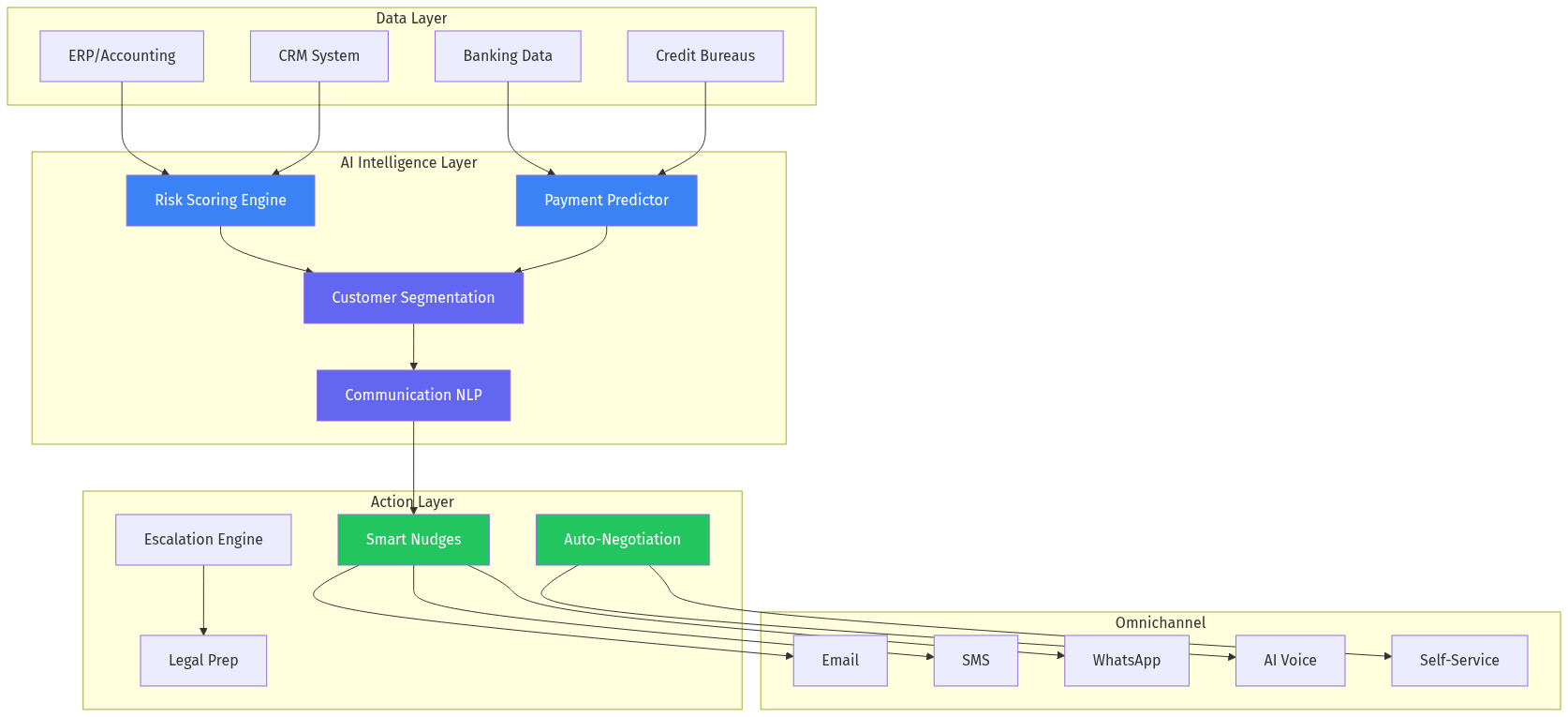

Applying Zeroth Principles: Before accepting "collections is adversarial," we question the axiom itself. Why must getting paid damage relationships? The core need isn't aggressive pursuit — it's information asymmetry resolution. Buyers often want to pay but face cash flow timing, invoice disputes, or approval bottlenecks. AI can surface these issues proactively and resolve them before they become delinquencies.This creates a $47 billion opportunity for AI-powered collections intelligence that predicts payment behavior, personalizes outreach, and automates negotiation — transforming AR teams from debt collectors into payment facilitators.