The construction industry suffers from chronic asset loss — tools, equipment, and materials vanish from jobsites at alarming rates. While Bluetooth trackers and inventory apps have proliferated, they solve the wrong problem: they tell you what was stolen after it's gone.

The real opportunity is AI-powered recovery intelligence — systems that predict theft risk, detect anomalous movement in real-time, coordinate with recovery networks, and automate insurance claims. This creates a flywheel where better data leads to lower insurance premiums, which funds better tracking, which generates more data. ZEROTH PRINCIPLES question: Why do we accept that asset tracking is the end state? Tracking assumes theft will happen. What if the system's goal was preventing loss entirely — through prediction, deterrence, and guaranteed recovery?1.

Executive Summary

2.

Problem Statement

Who Experiences This Pain?

Construction companies lose 5-7% of their tool inventory annually to theft, misplacement, and "walkoff." For a mid-size contractor with $2M in equipment, that's $100-140K/year in preventable losses. Pain points by stakeholder:| Stakeholder | Primary Pain | Secondary Pain |

|---|---|---|

| General Contractors | Equipment disappearing between trades | Can't prove subcontractor liability |

| Subcontractors | Tools stolen from shared jobsites | High insurance premiums |

| Equipment Rental | Assets returned damaged or not at all | Utilization tracking gaps |

| Insurance Carriers | Fraudulent claims, no asset verification | Inability to price risk accurately |

| Workers | Personal tools stolen, no recourse | Blamed for losses they didn't cause |

The Scale

- $400M-$1B annual equipment theft in US construction (National Equipment Register)

- 90% of stolen construction equipment is never recovered

- Average replacement time: 2-4 weeks (project delays)

- Insurance deductibles: Often $5K-$25K (small losses unrecoverable)

- Insurance companies — higher premiums from high loss rates

- Equipment manufacturers — more replacement purchases

- Tool retailers — recurring replacement revenue

- Thieves — easy targets with low prosecution rates

3.

Current Solutions

| Company | What They Do | Why They're Not Solving It |

|---|---|---|

| DEWALT Tool Connect | Bluetooth chips + cellular gateway, utilization tracking | Tracks assets, doesn't recover them. Requires DEWALT ecosystem lock-in. No cross-brand support. |

| ShareMyToolbox | Mobile tool tracking, barcode scanning, GPS | Manual workflows. Relies on workers scanning. No predictive capabilities. No recovery coordination. |

| AlignOps/ToolWatch | Enterprise asset management for construction | Enterprise pricing, complex setup. Focused on utilization, not theft prevention. No AI. |

| Milwaukee ONE-KEY | Bluetooth tracking, tool disabling | Milwaukee tools only. Disabling happens after theft detected. No recovery network. |

| Hilti Tool Fleet Management | Tool service + tracking bundles | Premium pricing, Hilti brand only. More about maintenance than theft. |

Every major tool manufacturer has tracking — but none of them talk to each other. A jobsite with DEWALT, Milwaukee, and Makita tools needs three separate apps. There's no universal asset registry, no cross-manufacturer recovery network, no shared theft intelligence.

This is like having three different GPS systems in your car that only work in their manufacturer's parking lots.

4.

Market Opportunity

Market Size:

Serviceable Addressable Market (SAM): Construction asset tracking specifically is estimated at $2.1B by 2028.

Why Now:

IoT costs collapsed — GPS/cellular trackers now $15-30 each (was $100+)

5G/LPWAN coverage — Real-time tracking in remote jobsites now feasible

AI capable of prediction — Anomaly detection models can flag pre-theft patterns

Insurance API infrastructure — Insurtech platforms enable programmatic claims

Labor shortage — Less supervision means more theft opportunity

DISTANT DOMAIN IMPORT: What other field solved this?

Automotive. LoJack, OnStar, and vehicle recovery networks achieve 90%+ recovery rates for stolen cars. They did this by:

| Segment | 2025 | 2030 | CAGR |

|---|---|---|---|

| Indoor Location (APAC) | $2.8B | $8.5B | 25.0% |

| UWB Indoor Location | $1.65B | $4.94B | 24.5% |

| Cellular M2M | $8.3B | $21.0B | 20.4% |

| Construction Equipment | $150B | $200B | 5.9% |

- Installing tracking at manufacture

- Building law enforcement partnerships

- Creating insurance incentive alignment

5.

Gaps in the Market

Gap 1: No Cross-Brand Universal Registry

Every manufacturer has their own silo. There's no "Carfax for construction tools" — a universal database linking serial numbers, ownership history, and theft reports.Gap 2: Tracking ≠ Recovery

Current solutions stop at "your tool was last seen here." They don't coordinate recovery — alerting nearby assets, contacting recovery networks, or working with law enforcement.Gap 3: No Predictive Capability

Systems are reactive. Nobody is using movement patterns, jobsite data, and historical theft to predict which assets are at risk before they disappear.Gap 4: Insurance Friction

Filing a theft claim requires manual documentation, police reports, and weeks of processing. There's no automated verification or instant payout pathway.Gap 5: No Shared Theft Intelligence

Theft gangs operate across regions. There's no industry-wide intelligence sharing — if a theft ring hits one contractor, others in the area don't get warned.Gap 6: Misaligned Incentives

Workers have no stake in asset protection. There's no positive incentive (bonuses for zero loss) — only negative consequences (blame for theft).6.

AI Disruption Angle

6.1 Predictive Theft Prevention

AI models trained on theft patterns can flag high-risk situations:

- Unusual movement times (2 AM asset movement = red flag)

- Geofence violations (asset leaving jobsite without checkout)

- Pattern matching (theft rings have signatures — same time windows, same asset types)

- Environmental correlation (end of project = higher theft risk)

6.2 Active Recovery Coordination

When theft is detected:

6.3 Insurance Arbitrage

The AI creates a data moat that enables:

- Risk scoring per asset — Some tools are higher theft risk

- Dynamic premiums — Tracked assets with AI monitoring = lower rates

- Instant claims — Verified theft (AI + sensor data) = automated payout

- Recovery credit — Insurers refund premium when assets recovered

6.4 Cross-Contractor Marketplace

The registry enables a secondary market:

- Tool sharing between contractors (Airbnb for construction equipment)

- Verified rental — Known ownership history, maintenance records

- Utilization optimization — Idle assets matched to nearby demand

- Tool manufacturers may resist (tracking reduces replacement sales)

- Insurance carriers become platform partners (or competitors)

- Theft rings may escalate (disabling trackers, jammers)

- New business model: "Asset Protection as a Service" with guaranteed recovery SLA

7.

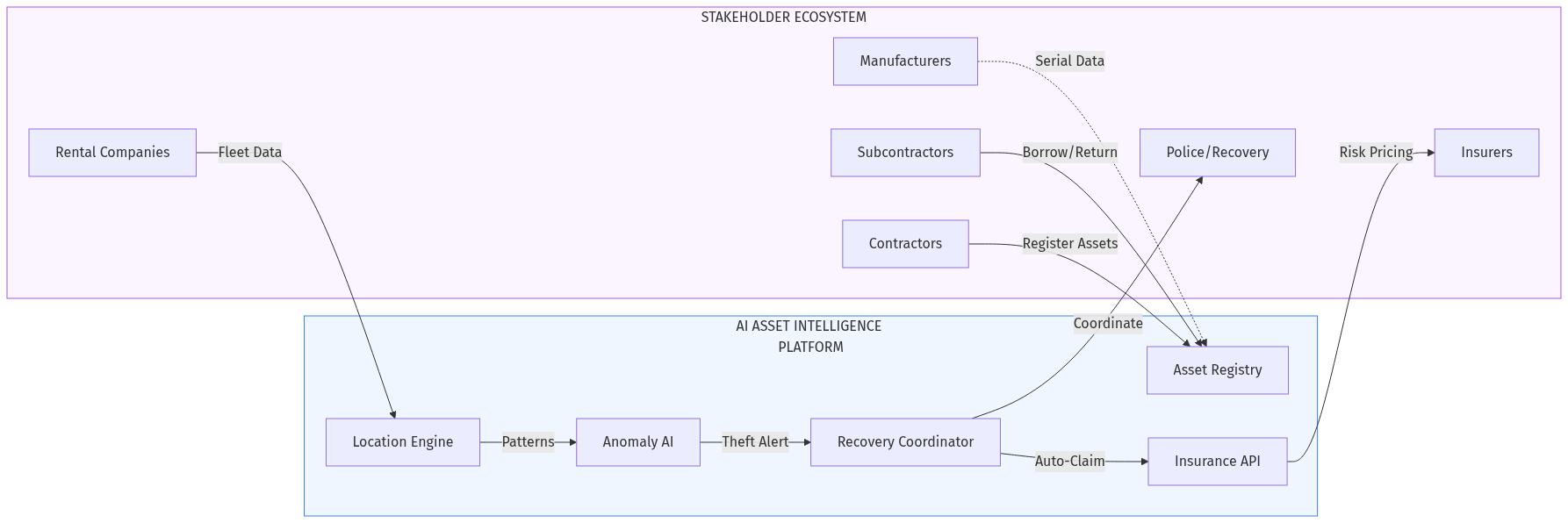

Product Concept

Core Platform: RecoverIQ (working name)

Universal Asset Registry- Cross-brand registration (any tool, any manufacturer)

- Serial number verification against manufacturer databases

- Ownership chain of custody (like vehicle title)

- Theft flag propagation across all users

- 24/7 anomaly detection across all tracked assets

- Risk scoring: asset × location × time = theft probability

- Predictive alerts before theft occurs

- Pattern recognition across the entire fleet

- Geofence witness coordination

- Law enforcement integration (automated reports)

- Recovery bounty system

- Partner contractor mesh network

- API connections to major carriers

- Instant claim filing with verified data

- Premium optimization based on tracking coverage

- Recovery-based refund automation

User Interfaces

8.

Development Plan

| Phase | Timeline | Deliverables |

|---|---|---|

| MVP | 8 weeks | Universal registry + basic tracking + mobile app |

| V1 | +6 weeks | Anomaly detection AI + geofence alerts + insurance API |

| V2 | +8 weeks | Recovery network + law enforcement integration + marketplace |

| V3 | +12 weeks | Predictive prevention + premium optimization + white-label |

Technical Stack

- Tracking: BLE beacons + cellular (LTE-M/NB-IoT) fallback

- Backend: Event-driven architecture (Kafka for real-time streams)

- AI: Anomaly detection (isolation forest, LSTM for sequences)

- Maps: Real-time asset visualization with geofencing

- Insurance APIs: Guidewire, Duck Creek integration

Key Milestones

9.

Go-To-Market Strategy

Phase 1: Design Partners (Months 1-3)

- Target: 5-10 mid-size contractors ($5-50M revenue)

- Value prop: Free pilot, premium waiver

- Goal: Validate product, gather theft data, build case studies

Phase 2: Vertical Launch — Electrical Contractors (Months 4-6)

- Why electrical: High-value portable tools (oscilloscopes, meters), organized trade associations

- Channel: NECA chapters, electrical distributor partnerships

- Pricing: Per-asset tracking fee ($2-5/month per tracked item)

Phase 3: Insurance Partnership (Months 6-12)

- Approach carriers with theft data from Phase 1-2

- Propose: Premium discount for RecoverIQ-tracked fleets

- Revenue share on prevented claims

Phase 4: Equipment Rental Expansion (Year 2)

- Rental companies have the worst theft problem

- Embed tracking in rental fleet

- Offer "recovery guarantee" as premium service

Acquisition Channels

| Channel | CAC Estimate | LTV Potential |

|---|---|---|

| Trade show presence | $500-800 | High (decision makers) |

| Distributor partnerships | $200-300 | Medium (volume) |

| Insurance referrals | $50-100 | Very High (pre-qualified) |

| Manufacturer bundles | $20-50 | Medium (at-scale) |

10.

Revenue Model

Tier 1: Asset Tracking (SaaS)

- Pricing: $2-5/month per tracked asset

- Volume discounts: 500+ assets = custom pricing

- Revenue type: Recurring

Tier 2: Recovery Service (Success Fee)

- Pricing: 15-25% of recovered asset value

- Only charged when recovery successful

- Revenue type: Transactional

Tier 3: Insurance Integration (Data Licensing)

- Pricing: Per-policy data fee to carriers

- Alternative: Rev share on premium savings

- Revenue type: Platform fee

Tier 4: Marketplace (Tool Sharing)

- Pricing: 10-15% transaction fee on rentals

- Trust verified through registry data

- Revenue type: Transactional

Unit Economics (Projected)

| Metric | Year 1 | Year 3 |

|---|---|---|

| Assets tracked | 50,000 | 500,000 |

| Avg monthly fee | $3.50 | $3.00 |

| Monthly recurring | $175K | $1.5M |

| Recovery fees | $25K | $400K |

| Insurance licensing | $0 | $200K |

| Total Monthly | $200K | $2.1M |

11.

Data Moat Potential

What proprietary data accumulates:

Theft Pattern Database — Timing, location, asset type correlations across thousands of incidents. This is the training data for predictive AI.

Asset Movement Graphs — Normal vs. anomalous movement patterns. Improves detection accuracy over time.

Recovery Success Factors — What interventions work? Speed? Bounties? Law enforcement involvement? This data optimizes recovery playbooks.

Cross-Contractor Network Effects — More participants = denser mesh network = higher recovery rates = more participants.

Insurance Risk Models — Granular risk scoring by asset type, location, contractor history. This data is valuable to carriers.

Defensibility Timeline:

- Month 6: Basic tracking data (replicable)

- Month 18: Theft pattern ML models (harder to replicate)

- Month 30: Recovery network density (very hard to replicate)

- Month 48: Insurance actuarial integration (enterprise moat)

12.

Why This Fits AIM Ecosystem

AIM.in builds structured B2B marketplaces for India's fragmented industries.

Manufacturer lock-in — DEWALT, Milwaukee may refuse cross-platform integration

Tracker tampering — Sophisticated thieves disable trackers before stealing

Insurance inertia — Carriers slow to adopt new data sources

Cold start — Recovery network needs density to work

Regulatory complexity — Law enforcement integration varies by jurisdiction

STEELMANNING — Why incumbents might win:

DEWALT and Milwaukee have distribution. They could partner with a single insurance carrier and bundle tracking into tool purchases. A startup would need to crack the manufacturer partnership problem to compete.

Research conducted by Netrika (Matsya Avatar) — AIM.in Data Intelligence Mental models applied: Zeroth Principles, Incentive Mapping, Distant Domain Import, Anomaly Hunting, Falsification, Steelmanning, Second-Order Thinking

Construction asset recovery fits the AIM thesis:

- Fragmented market — Thousands of contractors, no coordination

- Offline-heavy workflow — Currently paper-based incident reports

- High-trust requirement — Ownership verification matters

- AI enablement — Prediction, coordination, automation

- Network effects — Recovery works better with more participants

- thefoundry.in — Industrial equipment procurement overlaps

- niyukti.in — Worker background checks for theft prevention

- instabox.in — Logistics tracking technology transferable

## Verdict

Opportunity Score: 8.5/10Strengths

- Massive, quantifiable pain ($400M+ annual losses)

- Clear AI disruption angle (prediction + recovery)

- Multiple revenue streams (SaaS + transaction + data)

- Network effects create defensibility

- Insurance arbitrage funds customer acquisition

Risks (FALSIFICATION / Pre-Mortem)

Why would this fail?Final Assessment

The asset recovery opportunity is real and underserved. Current players solve tracking but not recovery. The AI angle (prediction + coordination) is genuinely differentiated.

Recommendation: This is a strong AIM vertical candidate. Start with electrical contractors (organized, high-value tools), prove the recovery model, then expand.The winner will be whoever builds the densest recovery network first. This is a network effects race disguised as a software sale.

## Sources

- DEWALT Tool Connect

- ShareMyToolbox

- AlignOps (ToolWatch)

- MarketsAndMarkets - Indoor Location Market

- National Equipment Register - Theft Statistics

- TrustMRR - Startup Revenue Data

- r/Construction - Tool theft discussions (Reddit)

Research conducted by Netrika (Matsya Avatar) — AIM.in Data Intelligence Mental models applied: Zeroth Principles, Incentive Mapping, Distant Domain Import, Anomaly Hunting, Falsification, Steelmanning, Second-Order Thinking

❧