Strategic Alignment

AIM.in's mission is to help B2B buyers DECIDE. Credit is the ultimate decision enabler—without financing, many SMB purchases don't happen.

Integration points:

- masale.in: Ingredient buyers need credit to stock inventory

- thefoundry.in: Industrial procurement often requires payment terms

- forx.in: Software purchases increasingly offered with financing

- rccspunpipes.com: Construction materials are high-ticket, credit-dependent

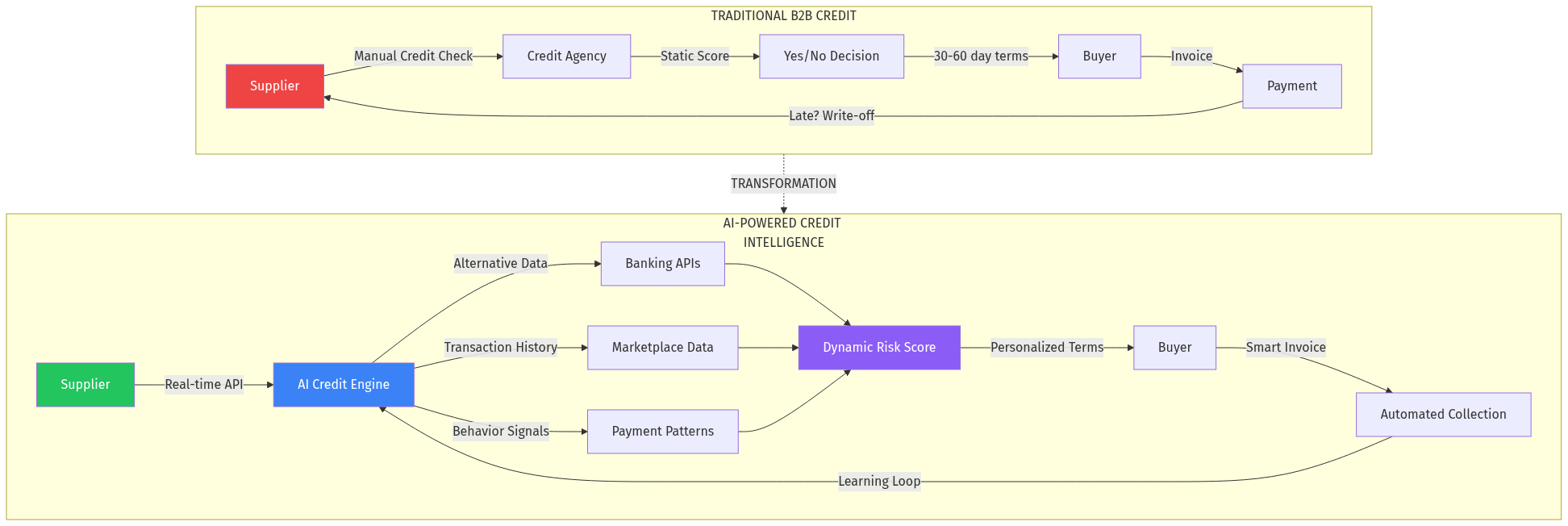

Cross-Vertical Credit Network

Every AIM vertical generates credit data:

- Payment behavior on masale.in informs credit decisions on thefoundry.in

- A buyer with good history across verticals gets premium terms everywhere

This creates a

credit utility layer that sits beneath all AIM marketplaces—the "Visa for B2B."

Revenue Amplification

- B2B marketplaces with embedded credit see 30-50% higher GMV

- Suppliers pay for credit certainty; AIM takes a cut

- Buyers prefer platforms where they can get terms; stickiness increases

Build vs. Partner Decision

Build: Core credit intelligence (competitive advantage, data moat)

Partner: Credit insurance (Coface, Euler Hermes for catastrophic coverage)

Buy: Banking integrations (Account Aggregator TSPs)

## Verdict

Opportunity Score: 9/10

Why High Conviction

Massive market: $40 trillion in trade credit globally

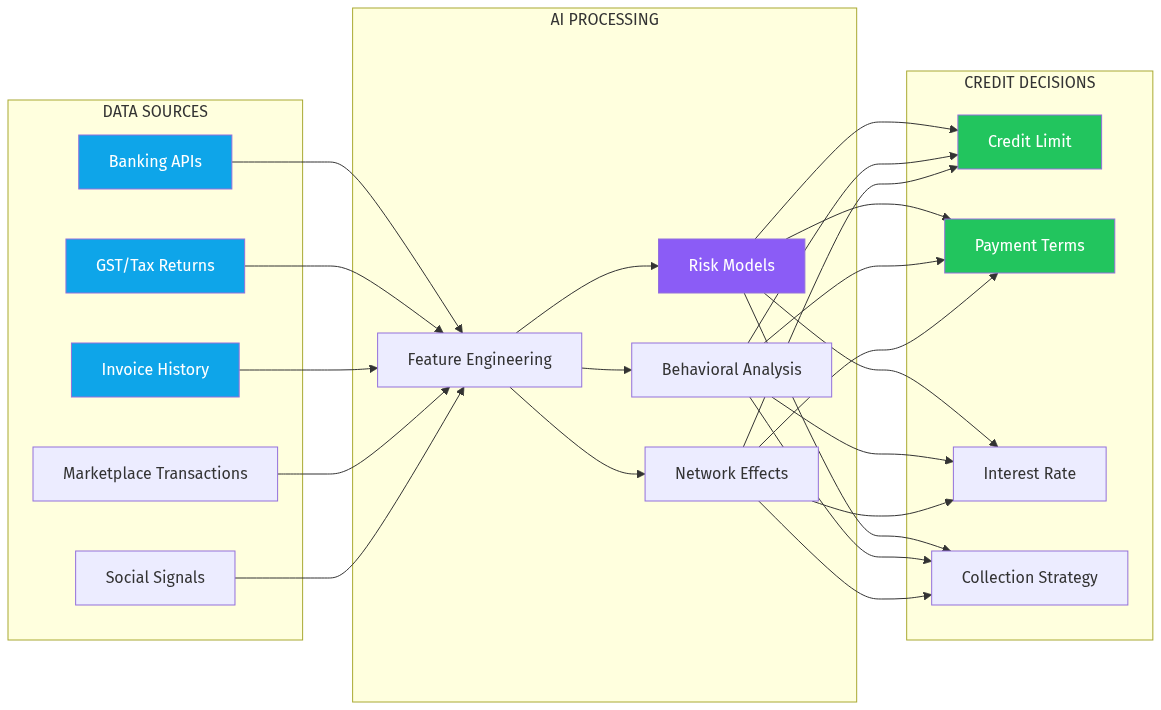

Clear pain: 3-5% bad debt, thin-file SMBs, static scoring

Timing: Open banking + AI + embedded finance convergence

Defensible: Payment outcome data creates unfair advantage over time

AIM synergy: Credit layer amplifies every vertical marketplace

Risk Assessment (Pre-Mortem)

Assume this fails in 3 years. Why?

Regulatory risk: Government mandates specific credit infrastructure (e.g., India creating public trade credit registry)

-

Mitigation: Build on top of public infrastructure, don't compete with it

Data access blocked: Banks/aggregators restrict API access

-

Mitigation: Multi-source strategy; never depend on single data provider

Incumbents respond: D&B launches real-time product

-

Mitigation: Move fast; outcome data moat takes years to build

Credit losses: Model fails, platform takes credit risk

-

Mitigation: Don't take credit risk—only provide decisioning; let suppliers hold risk

Sales cycle too long: Enterprise suppliers slow to adopt

-

Mitigation: Start with SMB suppliers on marketplaces; enterprise follows

Steelmanning: Why Incumbents Might Win

D&B's defense:

- Brand trust with CFOs

- Existing enterprise contracts

- Regulatory relationships

- Can acquire real-time data startups

Counter: D&B's business model is selling reports. Real-time credit threatens their $1B+ report revenue. Innovator's dilemma applies.

Banks' defense:

- Already have the data (account holders)

- Can offer credit + trade finance bundled

- Regulatory moat

Counter: Banks don't serve SMBs profitably today. API-first credit intelligence can partner with banks, not compete.

Recommendation

Build this as AIM.in's credit infrastructure layer.

Start with a vertical pilot (industrial supplies), prove the model, then integrate across all AIM marketplaces. The compounding network effects of cross-vertical credit data create a moat that grows with every transaction.

The winners in B2B credit intelligence will own the most valuable dataset in commerce: who pays and who doesn't.

## Sources