The Scope 3 Nightmare

Carbon emissions are categorized into three "scopes":

- Scope 1: Direct emissions from owned sources (factories, vehicles)

- Scope 2: Indirect emissions from purchased electricity

- Scope 3: Everything else—purchased goods, transportation, employee commuting, end-of-life treatment, investments

The cruel reality: Scope 3 typically represents 70-90% of a company's total carbon footprint, but it's entirely outside their direct control. A consumer goods company might have 50,000+ suppliers across 100+ countries, each with their own carbon profile that the company has zero visibility into.

Why Current Approaches Fail

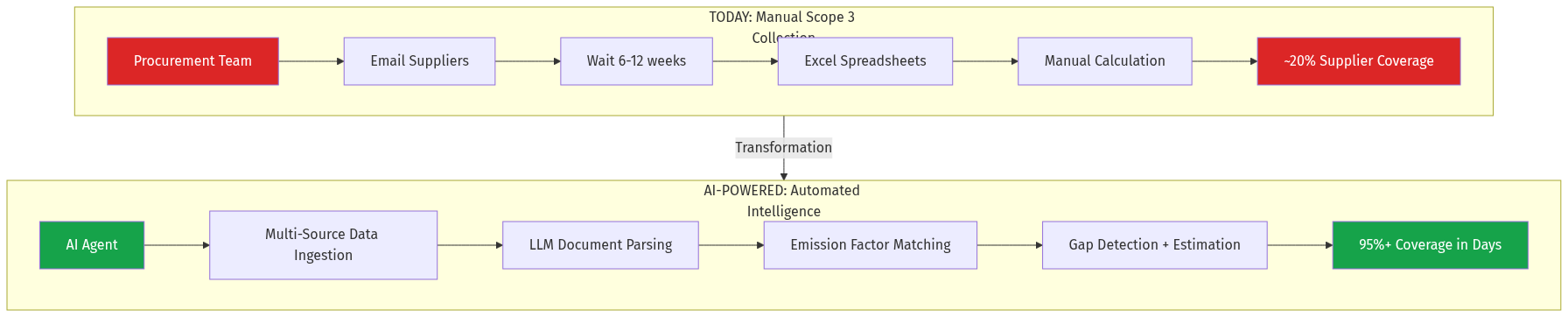

Manual supplier surveys achieve 15-25% response rates after months of follow-up. Suppliers don't have the data, don't understand the questions, or simply ignore requests from procurement.

Spend-based estimation (multiplying purchase amounts by industry average emission factors) produces wildly inaccurate numbers—often 2-5x off from actual emissions.

Consultants and auditors charge $2-5M annually for large enterprises and still deliver incomplete, outdated data.

The irony: Companies are spending millions to report numbers they know are wrong, to meet regulations designed to drive actual emission reductions.

Applying Zeroth Principles

"What fundamental axiom are we assuming that might be wrong?"

The assumption: Suppliers must provide their own emissions data.

But most suppliers—especially SMEs comprising 80%+ of global supply chains—don't know their emissions, can't calculate them, and never will invest in carbon accounting software.

The zeroth principle: The buyer's platform must calculate supplier emissions from available data (invoices, shipping records, utility bills, certifications) rather than waiting for suppliers to self-report.