The Indian SME lending market represents one of the largest AI transformation opportunities globally. With 63 million MSMEs contributing 30% of GDP but receiving less than 16% of formal credit, the gap isn't a lack of money — it's a lack of intelligence.

Traditional credit assessment relies on audited financials, collateral, and relationship banking — systems that structurally exclude small businesses. But three converging forces have created a perfect storm:

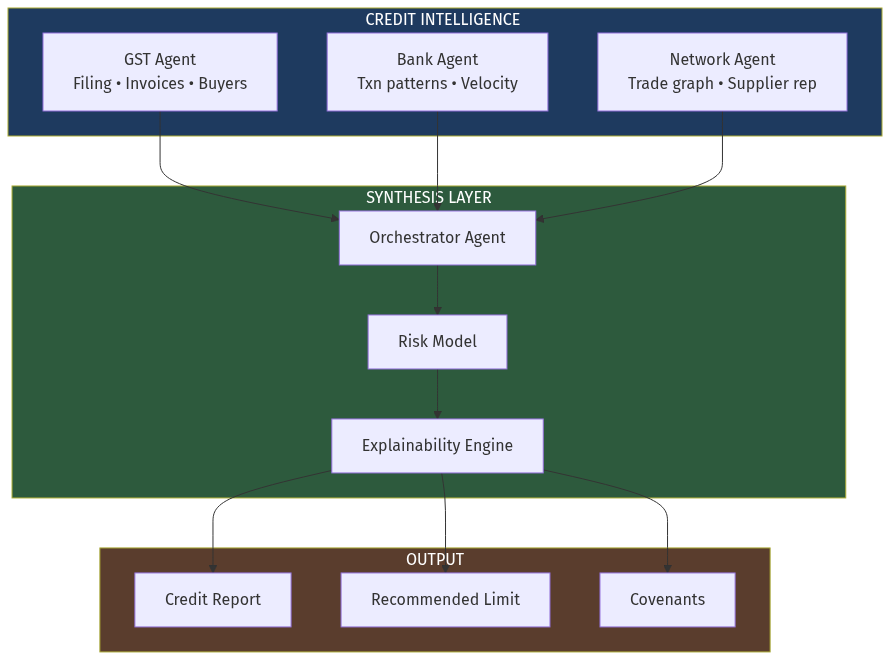

The opportunity: Build the "credit bureau for the informal economy" — AI infrastructure that converts transaction patterns, payment behaviors, and supply chain relationships into bankable creditworthiness signals.

slug: "credit" ---